Volatility Targeting is a simple concept. You set an annual volatility target for an asset, and adjust your exposure through time to meet that target. If your annual vol target is 10% and your measure of the asset’s volatility is 20%, you would hold 50% (10 divided by 20) of the asset to achieve the 10% vol. Mathematically, your vol target is the numerator and your denominator is the vol estimate. Most people either use implied volatility or trailing historic volatility as their vol estimate. The question arises: why bother?

Well this concept is to a large degree second nature in hedge fund portfolios where it is a necessity. If you have equal conviction that 2 year Note futures and S&P 500 futures are going to rise, you want them to have an equal impact on your PL. Buying equal dollar amounts of both is pretty dumb, because all the volatility in your portfolio will come from the equity future position. You have to either bring up the vol of your 2 year Note position to equal your S&P future position, or dial your equity down. Vol targeting enables greater diversification by allowing uncorrelated assets to have the same impact in a portfolio. This is the core idea behind risk-parity portfolios which use multiple assets.

In the last 10-15 years, this concept has entered into mainstream portfolio management. And with good reason. It works, though its popularity or overuse are now its biggest danger. In general, the version employed in Mutual Fund and ETF land is more constrained—hedge funds don’t have an issue leveraging up 2 year notes 20 times or more to be at the same vol as the S&P 500. Long only mutual fund managers are wary of levering anything more than 150%. There are more regulations and leverage is “bad optics,” as I once heard someone say. It is also within mainstream portfolio management that the idea has been applied more consistently to a single asset class, mostly equities, to be a tactical allocation decision device: putting more money into equities when equity vol is low, and less when vol is high.

Using the SPY ETF, shows the performance enhancements and side effects that come from the vol target pharmacy when applied to a single asset.

For our exercise we will examine the performance of two portfolios, the ETF SPY and our volatility target enhanced version of the same. Our volatility target is 1% daily vol or 15.8% annualized. Our vol estimate will use the trailing standard deviation of SPY over the last 200 days as the denominator. We can have a maximum position or leverage cap of 150% invested. We will rebalance every Monday at the close.

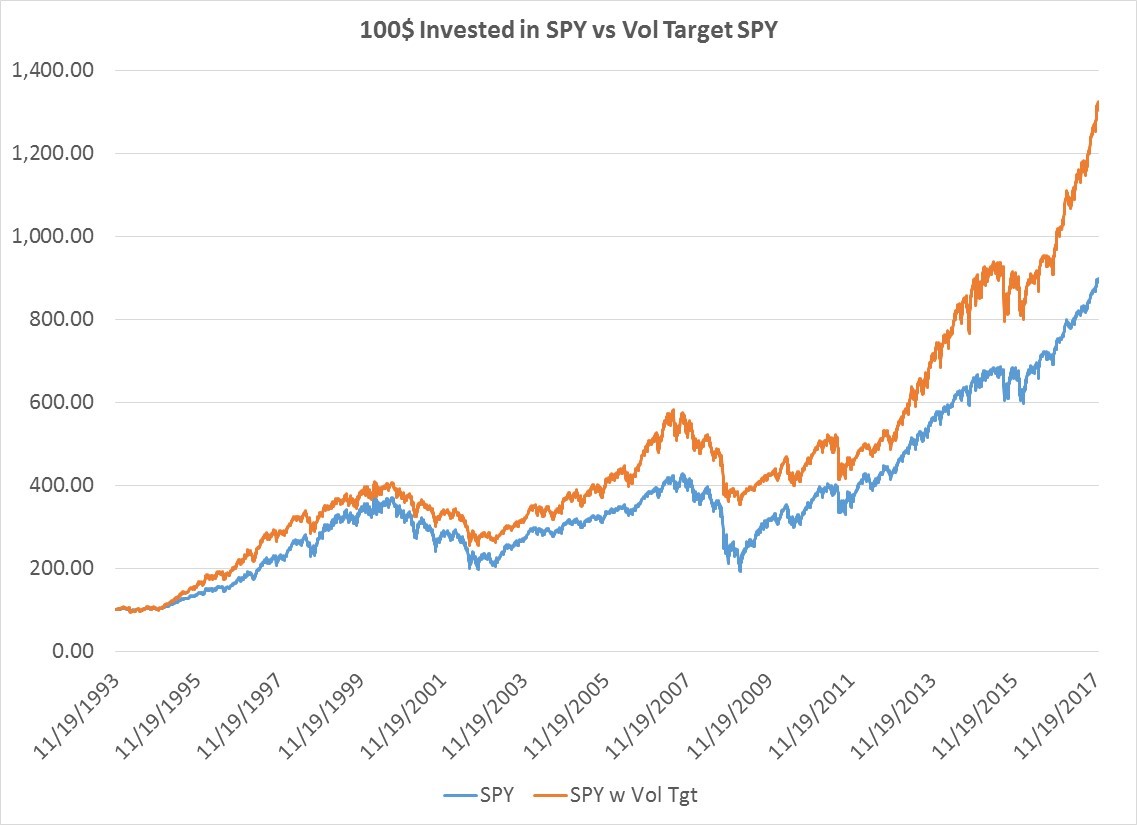

Below is the PL from both portfolios. Over time both portfolios do well, but the volatility target version offers better total returns.

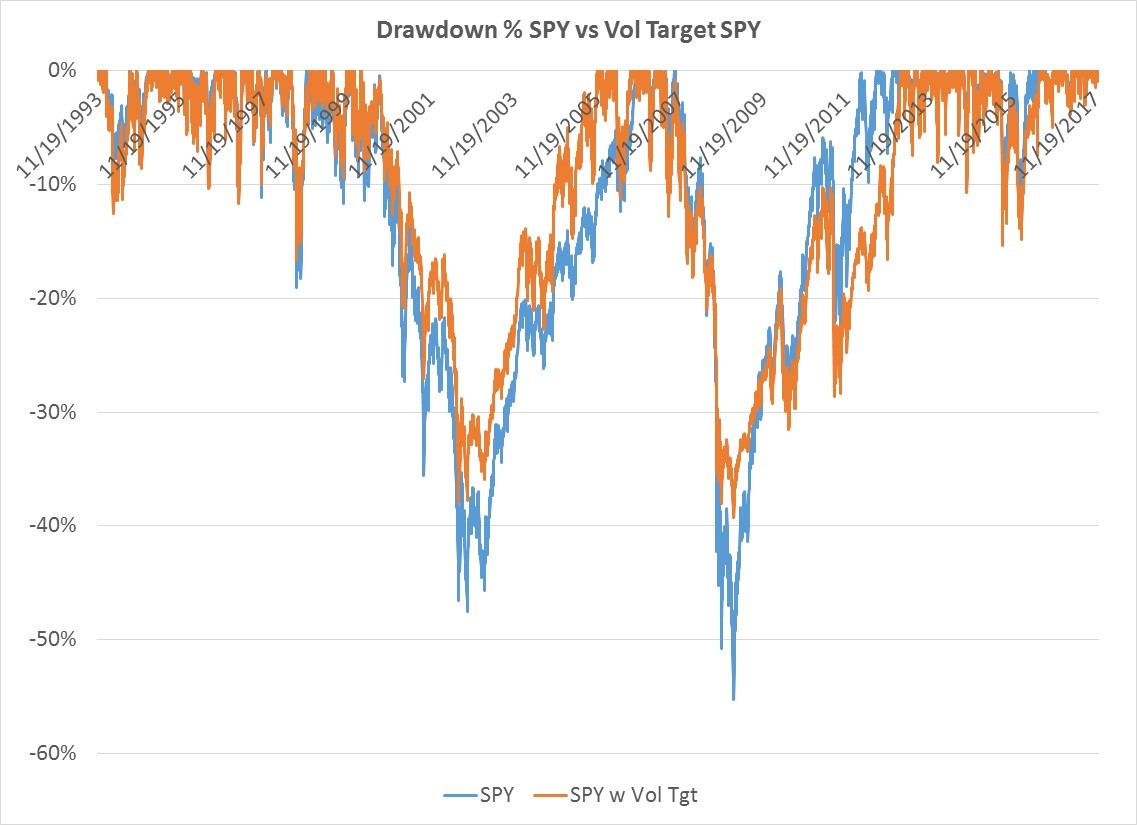

Here are the performance stats. When you look at risk-adjusted returns, the vol target portfolio is superior when you consider either the ratio of return to volatility or max loss.

| SPY | SPY Vol Tgt |

|

|---|---|---|

| Annual % Return | 10.8% | 12.1% |

| Annual Vol | 19% | 16% |

| Info Ratio | 0.58 | 0.74 |

| Max % Drawdown | -55% | -39% |

The vol target version of SPY experienced less painful maximum losses during the bear markets of 2003 and 2008.

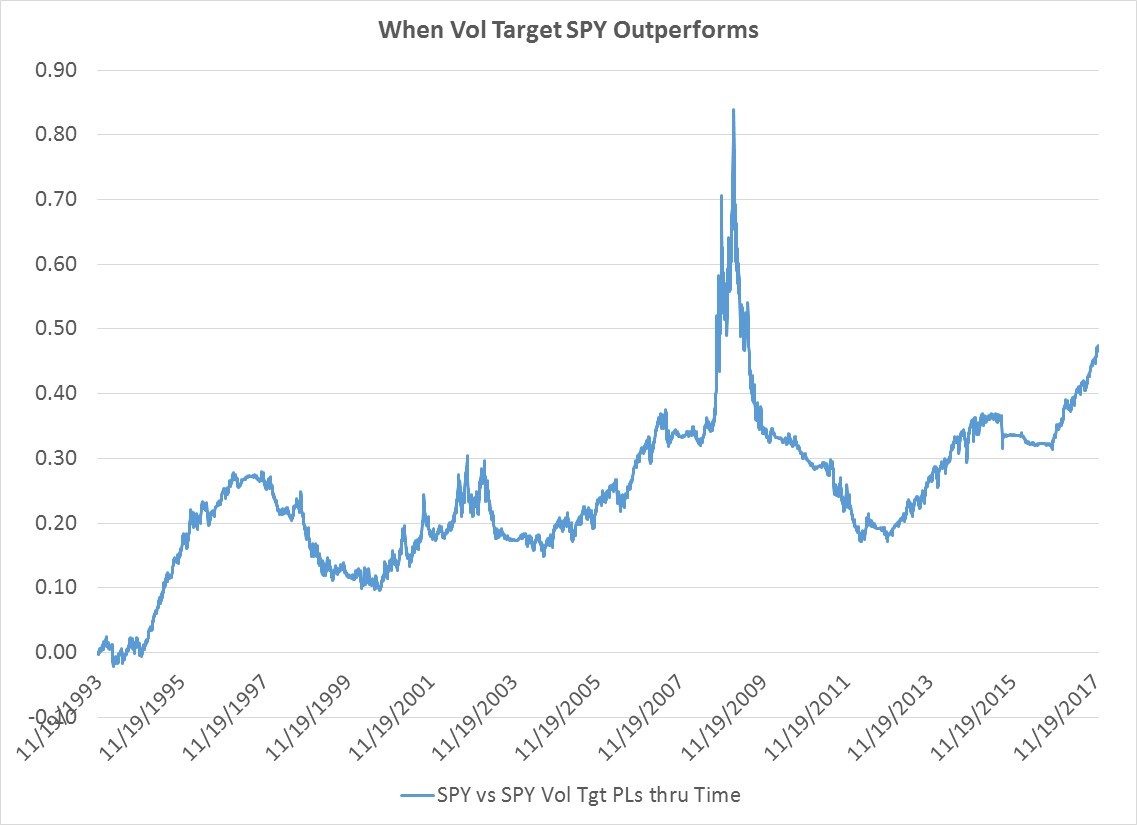

The last chart, and perhaps the most interesting, shows the relative out performance of the vol target strategy vs. SPY alone through time. What is apparent is that while it works, there are times when the vol target version of SPY really under-performs. Vol target SPY has been brilliant from 2012 to present as volatility has just gone to sleep and you are levering up in a bull market. The strategy also performed as designed going into the 2008 crisis, cutting risk as equities tanked. But consider the equity bubble in 1998 and 1999 when stock returns were incredible, but vol itself was very high and you dialed back your equity exposure. In this period you would have been much better off just buying SPY. The post 2008 crisis period was also terrible. Your trailing vol estimate combined with higher vol in general even in the implied vol market kept you dialed back in equities at a time that it would have been much better to just buy, and hold on for the ride. In a high vol, high return environs, vol targeting can look pretty bad.