Consumption growth matters a great deal in the developed world. It’s about 2/3rd of US GDP. So you would think there would be a pretty clear linkage between higher consumer growth rates, faster earnings growth and superior stock performance. Think again.

In fact, it’s quite the opposite.

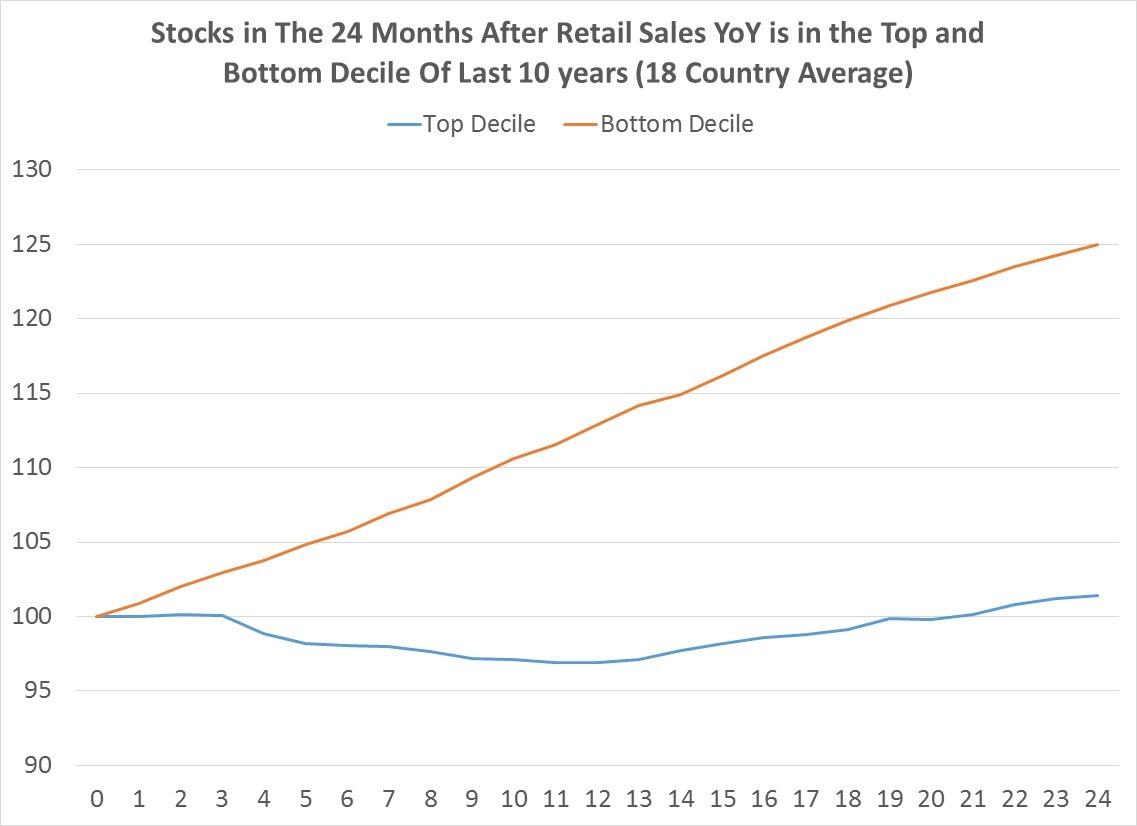

When you look at periods when annual retail sales growth was in the top decile and bottom decile over the last 10 years, and then measure subsequent stock returns, the bottom decile wins quite handily. The chart below shows an 18 developed country average since 1960 of stock index returns after annual retail sales growth was in the bottom or top decile over the prior decade.

We have some sample size here too. Between the 18 countries, there were 570 months when annual retail sales was in the top decile and 856 months when it was in the bottom decile. To prevent one country dominating, I simply took an equal average across all countries.

What the chart shows is not a subtle difference. When retail sales growth is in the bottom decile, you make, on average, just short of 25% over the next 2 years. Buy when its in the top decile, and you make a mere 1.43% over the next 24 months.

Why?

I don’t know but there are two probable explanations, both of which may be at play. Weaker growth leads to lower interest rates which begets borrowing and expansion. Higher growth leads to higher rates and things slow down. Markets are also discounting mechanisms and people aren’t real good at imagining a world different than the world they currently inhabit. So when consumption is weak, people and markets are overly pessimistic. Similarly, “happy days are here again” consumption is probably the period the market has become overly optimistic in its future pricing.

At present, only one country, France, sits in the top decile of 10 year retail sales growth. No one, unsurprisingly, is currently in the bottom decile.