Since the asset market crash in 2008, US monetary policy has been partly geared toward repairing domestic household balance sheets saddled with mortgage debt. Household liabilities, i.e., mortgage debt, needed to be brought back in line with the incomes and the assets that service that debt with sufficient monetary force to avoid the Depression. Not shockingly, the Fed dropped interest rates to zero and purchased assets like mad to keep the economic engine moving.

To a large extent, the Fed has now accomplished this goal. Households now have a lot more (low yielding) cash than they do mortgage debt, as you can see in the charts below. If US Households pooled their funds in aggregate they could simply repay all of their mortgage debt in one fell swoop by wiring money out of their bank and money market accounts.

Looking in more detail…

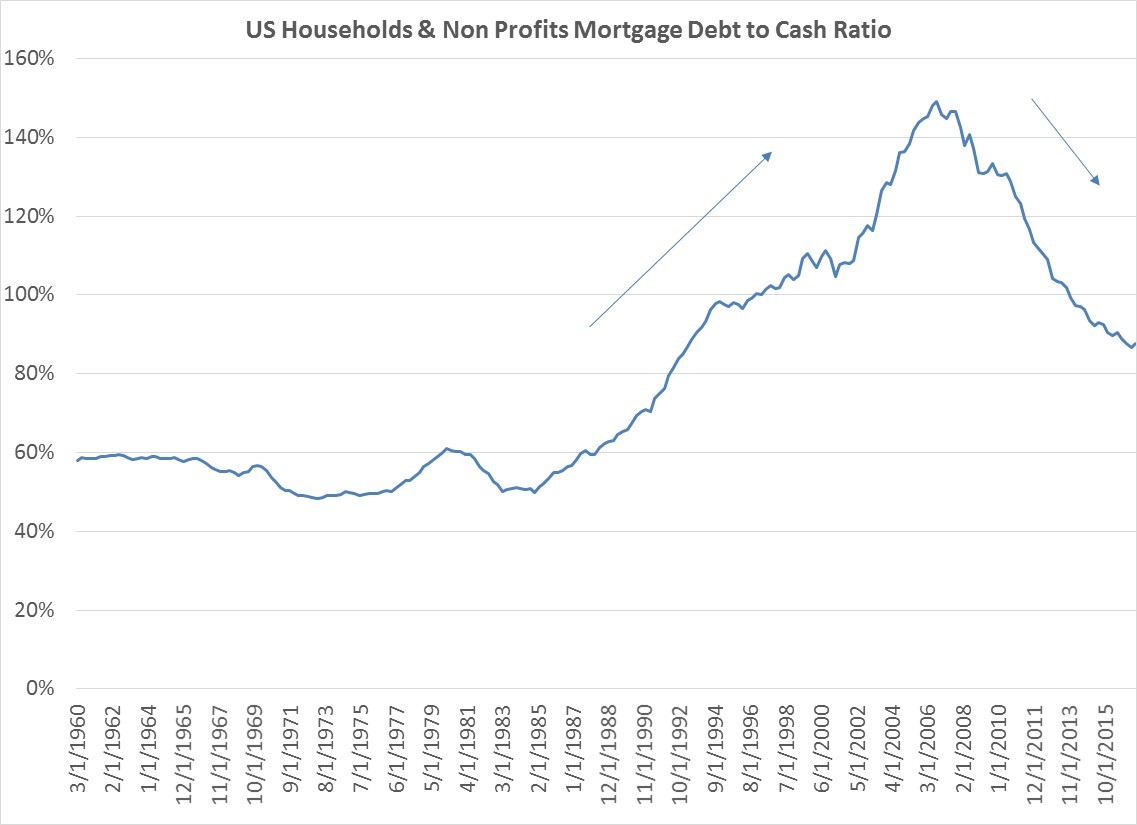

After being fairly steady from 1960 to 1988 at a ratio of around 60% mortgage debt to cash, households went on a borrowing binge for the next twenty years ending in 2007. Since 2008, that borrowing binge has been slowly rectified, as household mortgage debt peaked in the second quarter of 2008, and simultaneously household holdings of cash have steadily grown, such that ratio is now safely below 100% (its currently 88%). While not as modest and debt-light as the 60% level we saw in the 1960s, when all is said and done, households look to be in better financial shape now.

(Data source: US Federal Flow of Funds data for this all subsequent charts)

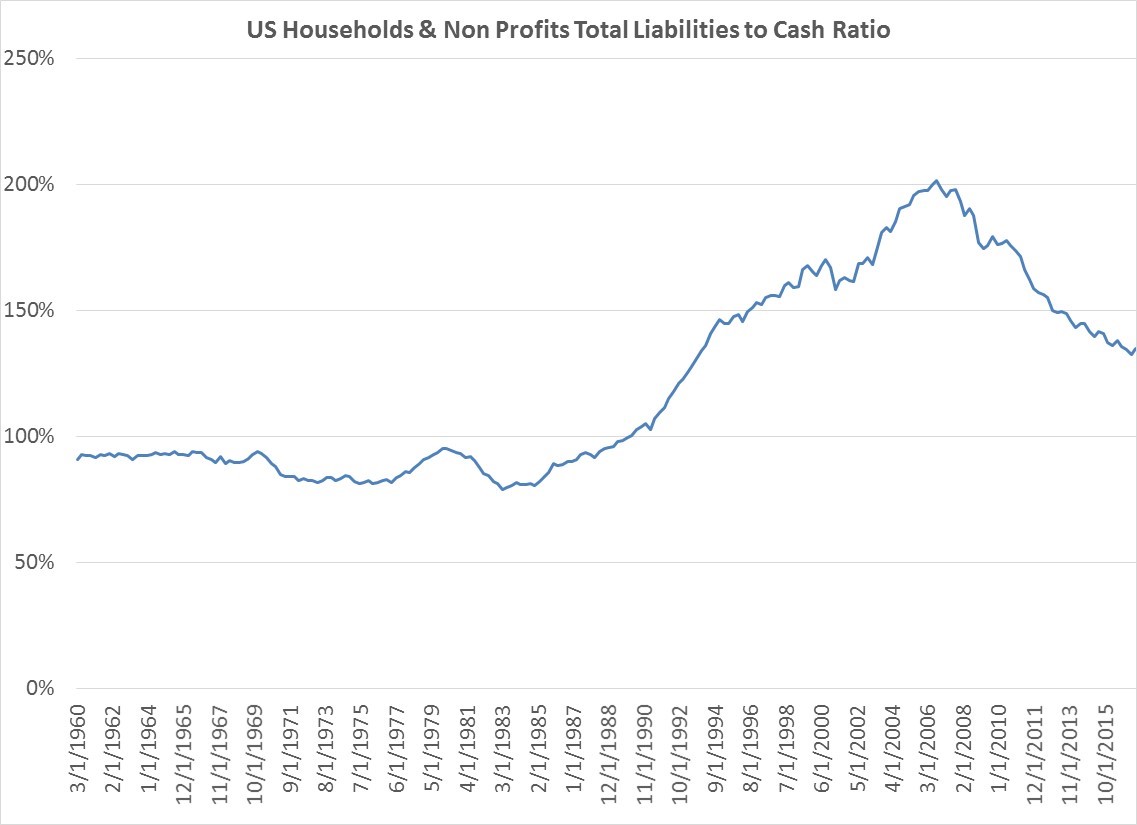

Not everything is rosy, however. We are simply using cash here as a proxy for liquid assets and ignoring holdings of stocks and bonds. When measured in this somewhat narrow way, total liabilities of US households remain fairly high. Again looking back at the prudent period before 1990, the ratio of total liabilities to cash was safely below 100%. That number peaked in 2008 above 200%, and lies around 135% now. This is a massive improvement, but it leaves some room to go, since household liabilities still exceed cash holdings.

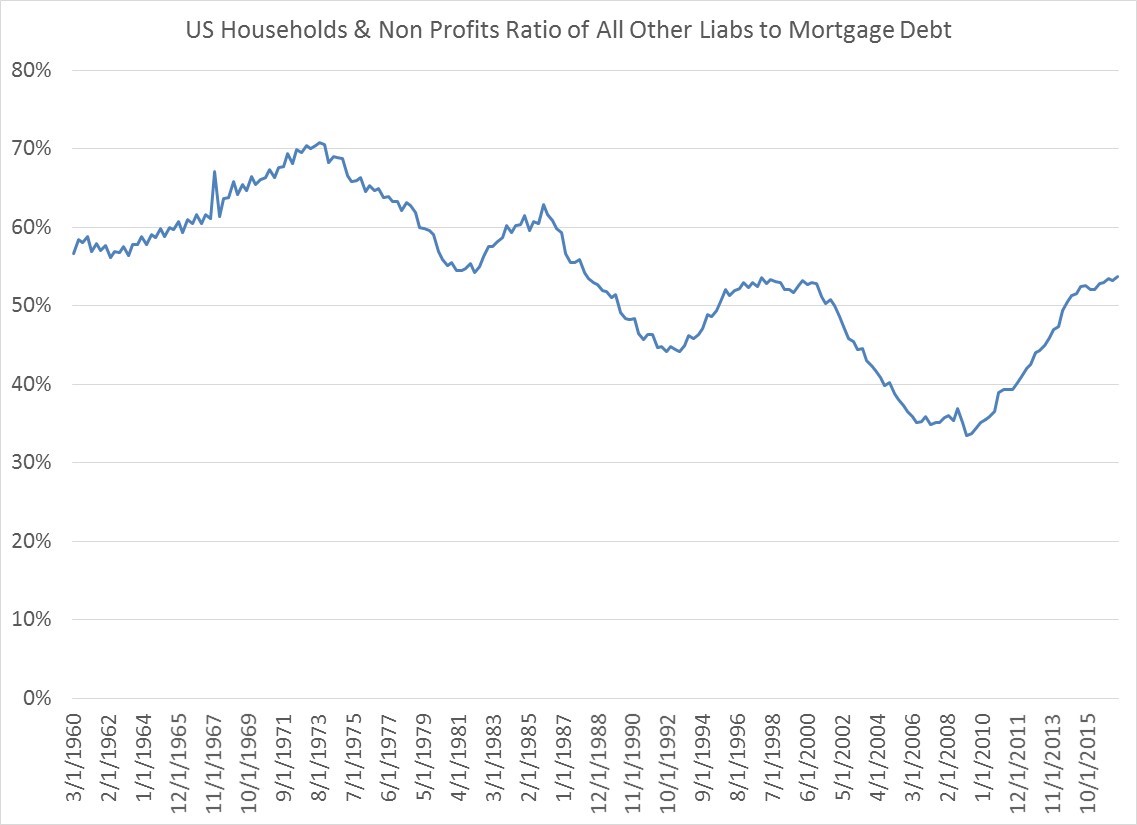

Additionally, the ratio of non-mortgage debt relative to mortgage debt for US households has been steadily rising since the peak in crisis as households have taken on more consumer credit debt: mortgage debt has contracted by $814 bn since the first quarter of 2008, while consumer credit has grown by $1.094 trn. For context, over the same time frame, cash has increased by $3.511 trn. So the increase in consumer credit through this lens is modest.

For the time being at least, these decade long trends look set to continue, though its quite possible that some of the household debt composition numbers may begin to shift in the coming years. Housing booms in certain cities and in California, if they get too out of hand, may increase household mortgage debt again. But in a broader sense, the balance sheet repair that was necessary after 2008 has to a large extend been accomplished.