The levels data from the US Flow of Funds has some fascinating information about the behavior of the major sectors of the US economy. Today we are going to take a quick look at some of the longer-term secular trends that have affected US non-financial corporations (meaning no banks, insurance companies etc. included).

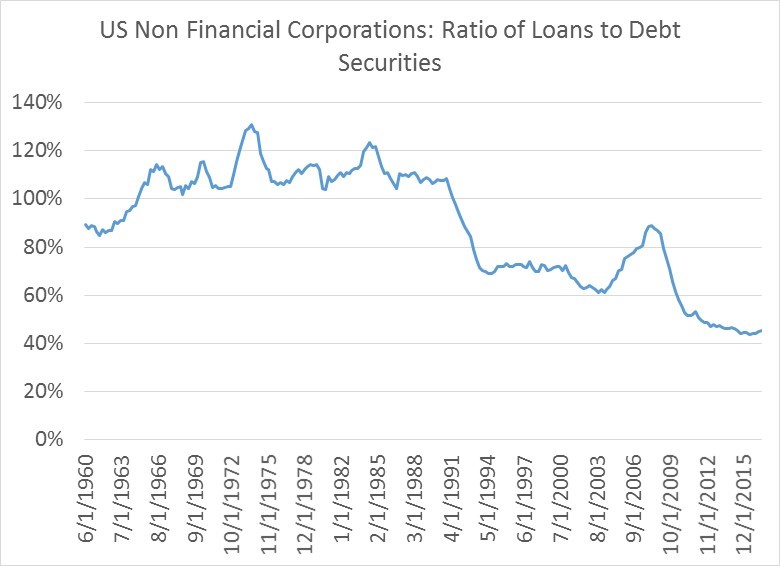

First, let’s look at the slow change that has happened in the way that US corporations borrow now vs. yesteryear. From 1960 until about 1990, corporate borrowing was pretty well balanced between issuing debt (via bonds, notes or paper) and bank loans—a number above 100% indicates corporations borrowed more from loans than by issuing debt, a number at 100% means the two were equal financing sources, and a number below 100% indicates debt issuance exceed loans. Since 1990, corporations simply stopped bothering going to their bankers to ask for a loan with the same frequency. We now live in a world where corporations actually borrow 2/3 rds of their funds by issuing debt, and derive only about a third from loan financing. Three Martini lunches over golf with commercial bankers have been replaced by abstemious and heavily regulated meetings with investment bankers.

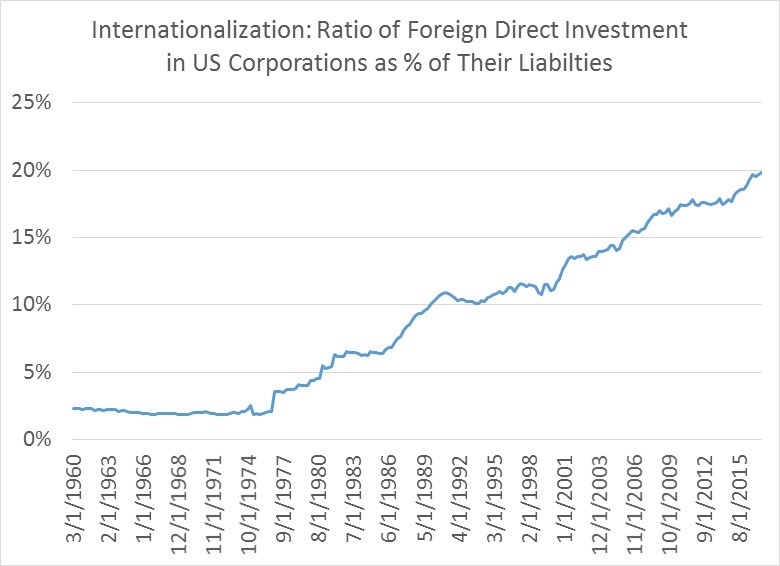

The second secular trend has been the steady inflow of foreign capital into this country. We hear the headlines about how Asian countries with current account surpluses like Japan and China are huge buyers of US Treasuries. What we hear less about how foreign direct investment in US corporations has now reached almost 20% of their “liabilities”. As a refresher, foreign direct investment or FDI means a foreigners either set up a factory or acquired ownership or a controlling interest in US business assets.

To a large extent this gradual uptrend appears to have been related to at the start at least the breakdown of bretton woods and the emergence of a free floating US dollar. But greater international trade and financial integration has also made it very easy for foreigners to invest in US corporations, which continue to appeal to people overseas. This a trend that seems to show no signs of stopping either. The US remains an attractive investment destination.

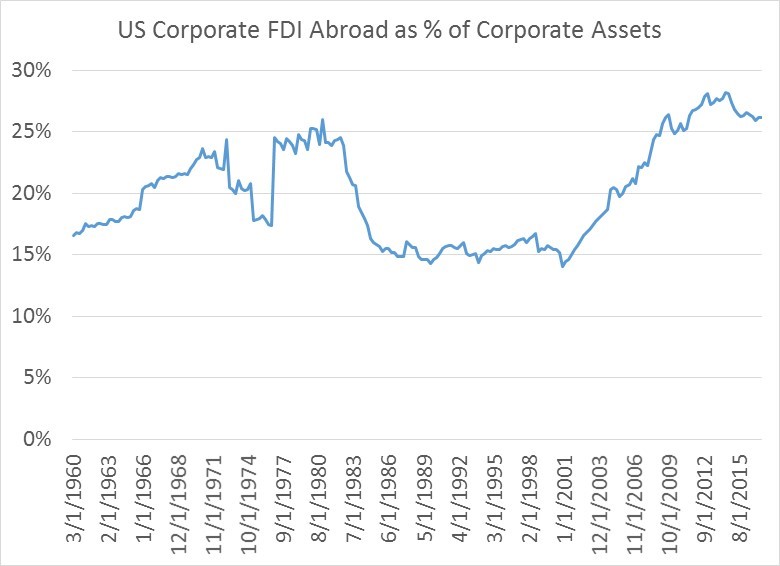

By contrast, US corporate direct investment abroad does not show the same continuous slope. Again with bretton woods in the early 1970s you do see a sustained spike in investment outside the US in the 1970s. But then in 1980s and 1990s only 15% of corporate assets are abroad, as US corporation seems to see better investment opportunities domestically. Probably because of the economic emergence of China, starting in the new century, corporations have put more money into factories there and in Asia and into acquiring overseas businesses.

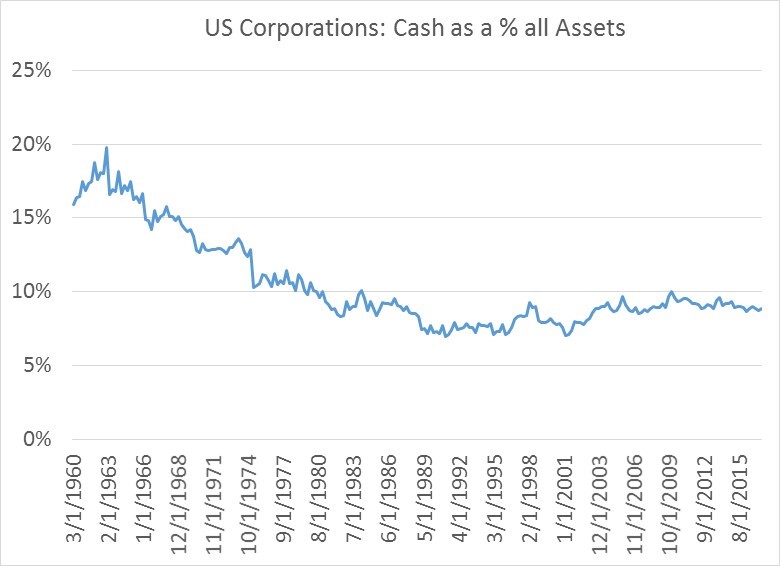

The final interesting trend is that US corporations, save Berkshire Hathaway and Apple, simply are not as cash-rich in aggregate as before. One would think that corporations would show some cyclical variability in their response to investment demand in their asset mix, hoarding a bit more cash when times were tough or the investment future was less certain. Nope. For thirty years from 1960 to 1990, cash as a % of assets simply declined steadily, before leveling off around 8% where it has remained roughly since with some minor variation since.