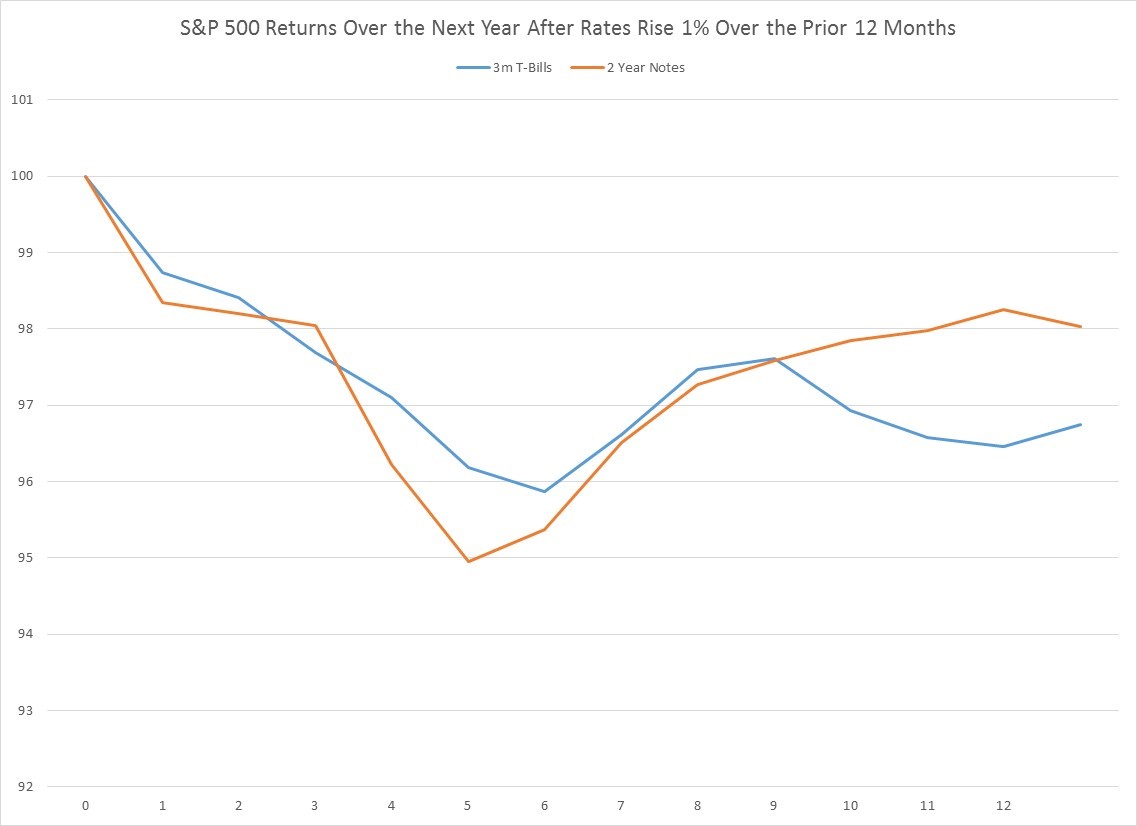

Over the last year, 3-month T-Bills and 2-year Notes have both gone from up about 100 basis points. In theory, higher interest rates should not be good for stocks. Higher rates curb economic demand and therefore sales growth and ultimately earnings growth, and simultaneously raise the cost of corporate borrowing which funds earnings. And when you look both in the US and across a large swathe of developed countries, this relationship holds. Put another way, the prospects for positive equity returns for the next 1-12 months in the US, if 1 year interest rate changes are your only guide, is negative.

Since 1960, annual changes in 3-month T Bills greater than 1% (with the annual change from the prior month being less than 1%) have occurred 21 times, using month-end data. One year changes greater than 1% for 2-year notes have happened 28 times over the last six decades. The first chart shows what equity returns look like, on average, in the next year after this rate increase. Results over the next year are negative with most of that decline occurring in the first 5 months. While this does not mean equities can’t go up in the US, it does mean that the statistical odds favor a decline.

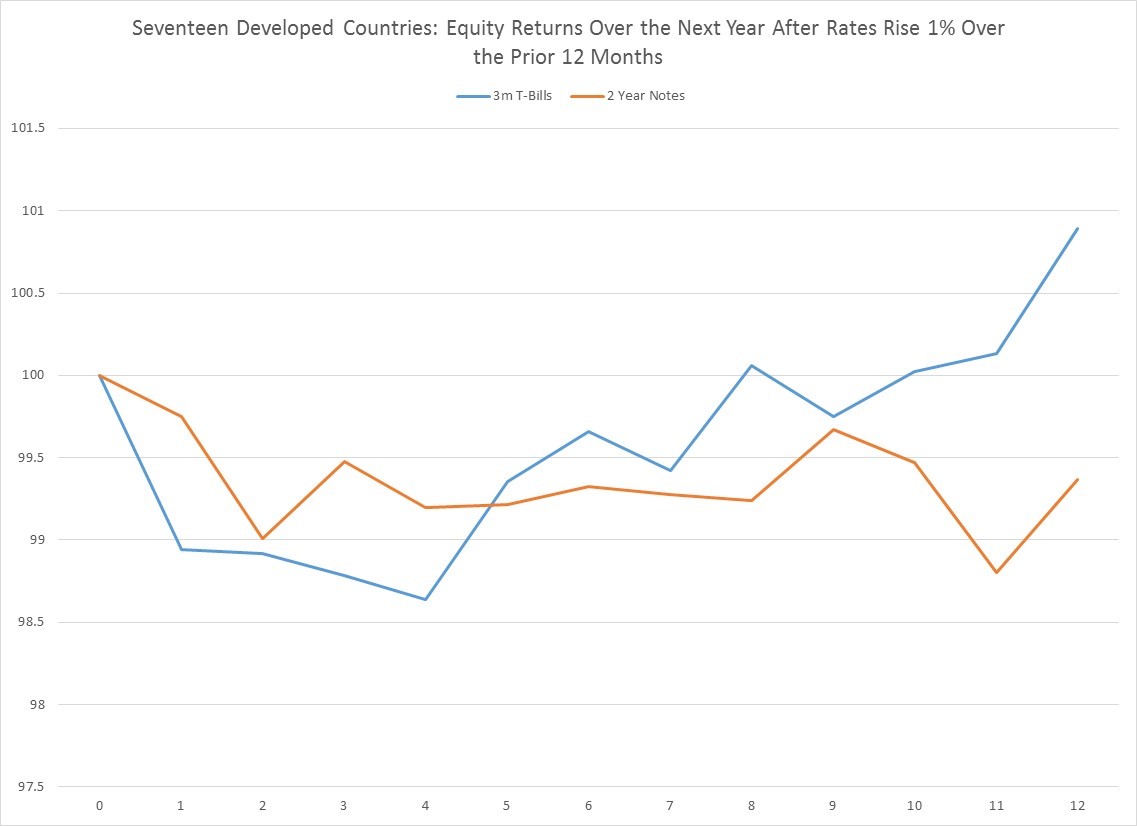

When you look at a much larger set of developed countries, the same relationship holds, only the statistical evidence is that much stronger (as you can see in the next chart). Over the last 6 decades, a +1% annual jump in rates has happened 258 times for 3 M bills, and 208 times for 2 year notes. As in the US, most of the negative returns occur in the first few months.

If the recent 1% annual jump in US rates is negative for domestic stocks on an absolute basis, the same is not true in the rest of the developing world. Only Canada, where annual changes in 2 year note recently passed above 1%, has seen rising rates on the same scale as the US. Outside North America no major developed economy is seeing rate hikes this quickly (some are actually declining), so there is a strong case selling North American equity in favor of other developed equity markets over the next few months.