This article was written with Chris Shuba and Joe Mallen of http://heliosdriven.com/ And has appeared here in ETF Trends

When considering how currencies affect US $ portfolios, one must think about four things:

- Buying a foreign currency asset is a bet that the US $ will decline.

- The longer-term contribution of currencies to portfolio returns and volatility can be substantial.

- Some currencies have hidden regime jumps or shock risks.

- Will the US $ decline or rise the currency you invest in.

First, quite unlike stocks or bonds, currencies have no inherent value, only relative value, and when you make a relative value investment, you bet on one instrument rising more than another. That is because a currency only has value relative to what it can be exchanged for, whether that is the Japanese Yen, Gold or Bitcoin. Thus, putting money in a foreign currency means that you are implicitly expecting that currency to rise relative to the dollar, or for the dollar to fall relative to the currency that you bought.

For example, when you buy a broad non-US ETF like JPMorgan Diversified Return International Equity ETF (JPIN), you assume that over time a diversified basket of global stocks will rise, and simultaneously assume that the US $ will fall in value. The changes in both the portfolio of stocks and the portfolio of exchange rates affect your $ PL. In the example given, let’s say it’s a global stock market holiday and every equity market in the world closes for a 4 day weekend, but the currency markets remain open. Over that long weekend, the value of the stocks in JPIN will remain unchanged, but a 3% decline in the value the US $ relative to the currencies in the ETF will cause the value of your investment in JPIN to increase by 3% in dollar terms.

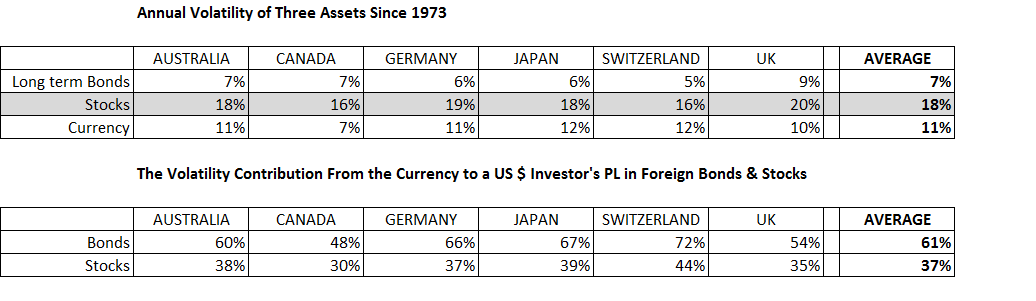

Second, while one might not think that exchange rates contribute to a long-term investment in an asset in another currency, the fact is they do. Consider the table below, which shows the annual volatility of the exchange rates of several countries vs. the US $, as well as the annual volatility of long-term bonds and stocks in the same country.

As you can see in the first table, Annual Volatility of Three Assets Since 1973, on average, the annual volatility of long-term (10 year) bonds in major developing countries has been about 7% vs. 11% for the currency. For stocks, the average annual volatility has been 18% vs. 11% for the currency. However, it is the second table, The Volatility Contribution From the Currency to a US $ Investor’s PL in Foreign Bonds & Stocks, that tells the real story. On average, 61% of a US investor’s foreign bond PL is determined by changes in the exchange rate, with only 39% coming from the performance of the bond itself. That is the majority. So, if you buy foreign bonds, it makes sense to hedge. With stocks, more than a third or 37% of a US investors PL is driven by the currency change. Put another way, 37% of your foreign stock PL is being determined by a factor that is extremely hard to predict.

Third, currencies occasionally make large, unexpected moves. These large changes are usually a currency devaluation relative to the US $, though not always. Latin American currencies, in particular, have a long and colorful history of dramatic collapse. Devaluations naturally cause a US $ investor to lose money on the currency part of their investment. Also, devaluations are usually inflationary and negatively impact holdings of local bonds, because local interest rates typically will rise. The impact of a currency shock on local equities is not always as predictable. Stocks that are highly dependent upon local or foreign currency debt, fall as rates rise and their foreign debt obligations increase, but an export company with little debt will likely see its share price skyrocket because the firm is now internationally more competitive.

For US investors, currency shocks are not always an emerging market issue. In the last few years, the UK and Switzerland have both experienced significant sudden changes in their currency value, because of the Brexit vote and an abrupt change in Swiss Central Bank policy. Should Denmark suddenly decide to uncouple the Krona from the Euro, or Hong Kong or China decide to make their currencies more free-floating, there would be massive changes in the exchange rate. These large potential changes in currency value, whether in emerging markets or the developing world are something investors need to be aware of.

Finally, one must consider the future direction of the US $. If it declines, foreign currency investments gain in dollar value, and if it rises, these same investments decline in dollars.

On the one hand, the US $ has some major pluses. For now, at least, it remains the world’s reserve currency. Our relative geographic isolation means the US is where funds typically come in times of geopolitical trouble.

US growth is strong relative to much of the developing world, which makes it attractive to capital seeking higher growth rates. And, the US Central bank is raising rates, so it is attractive from a relative interest rate perspective.

On the other hand, the US $ has declined a great deal vs some major trading partners over the last 40 years. In the 1970s, a dollar bought up to 360 Yen; now it buys 110. In the late 1980s, one US$ could buy 10 and even 12 Renminbi on the black market; now a dollar buys 6.5 Renminbi. Over the long-term, countries with high savings rates and current account surpluses tend to see their currency rise relative to countries with low savings rates and large current account deficits (who must fund their spending by importing capital from abroad).

The US Current Account is still in the red (though much smaller than several years ago), and US savings numbers have improved. That said, remember that currencies are a relative value investment. Compared to thrifty East Asia, the long-term US numbers are not as attractive. The fundamentals for the rest of the world relative to the US are not as crystal clear.

The US currency is also affected in the short-run by both current political policy and the business cycle. Trade wars and ballooning public deficits don’t inspire confidence among foreign investors. And if foreign investors choose to keep their money at home, it would cause the US $ to decline and US interest rates to rise.

Inflation and higher interest rates are the other related factors that will impact the US $ in the near term. As noted above, higher relative interest rates and relative growth rates have attracted foreign capital to the US. But if there is the perception that these higher rates of growth and yields are being eroded by uncontrolled inflation, and that the Federal government cannot control its spending and the Fed is behind the curve, foreigners will reduce their US investments. Inflation, when it is perceived to be too high, will cause a currency to lose value, because it destroys purchasing power. Unfortunately, trade wars as well as a decline in the US $ can further exacerbate inflation by making imports more expensive. To date, we have not seen a run on the dollar or inflation reach a dire tipping point that would drive interest rates up and asset values down, but the probability of this happening has increased.

Will the next 40 years look like the last 40 years for the US $? No one can know for certain. However, in a future post article, we will show how this gradual decline in the US $ has been one of the major benefits US $ investors have gained in the past by putting their money to work in foreign equities.

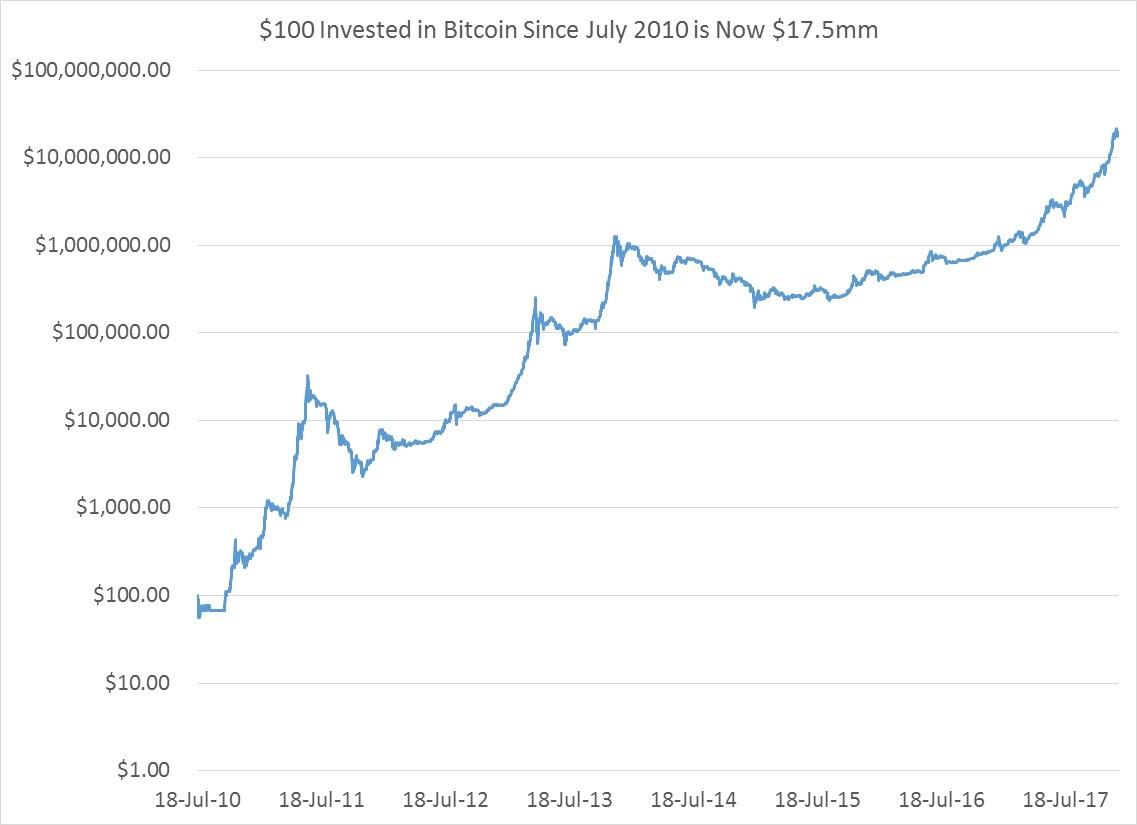

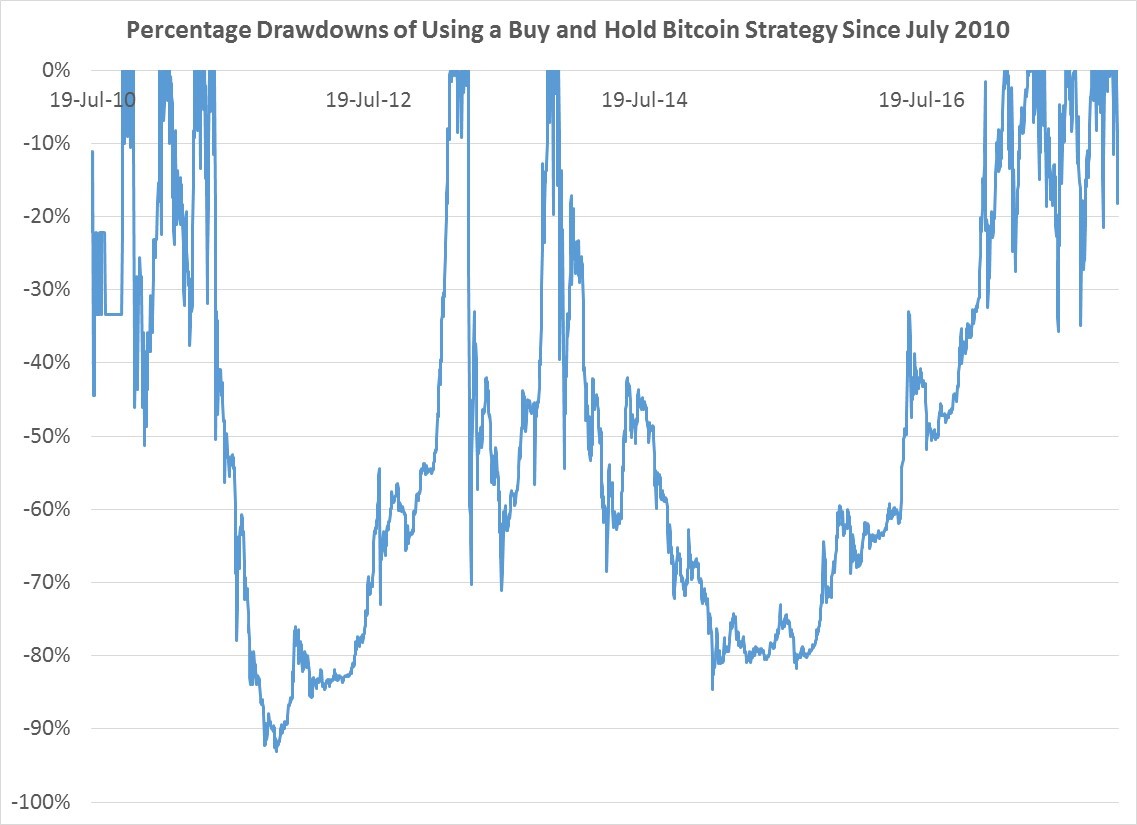

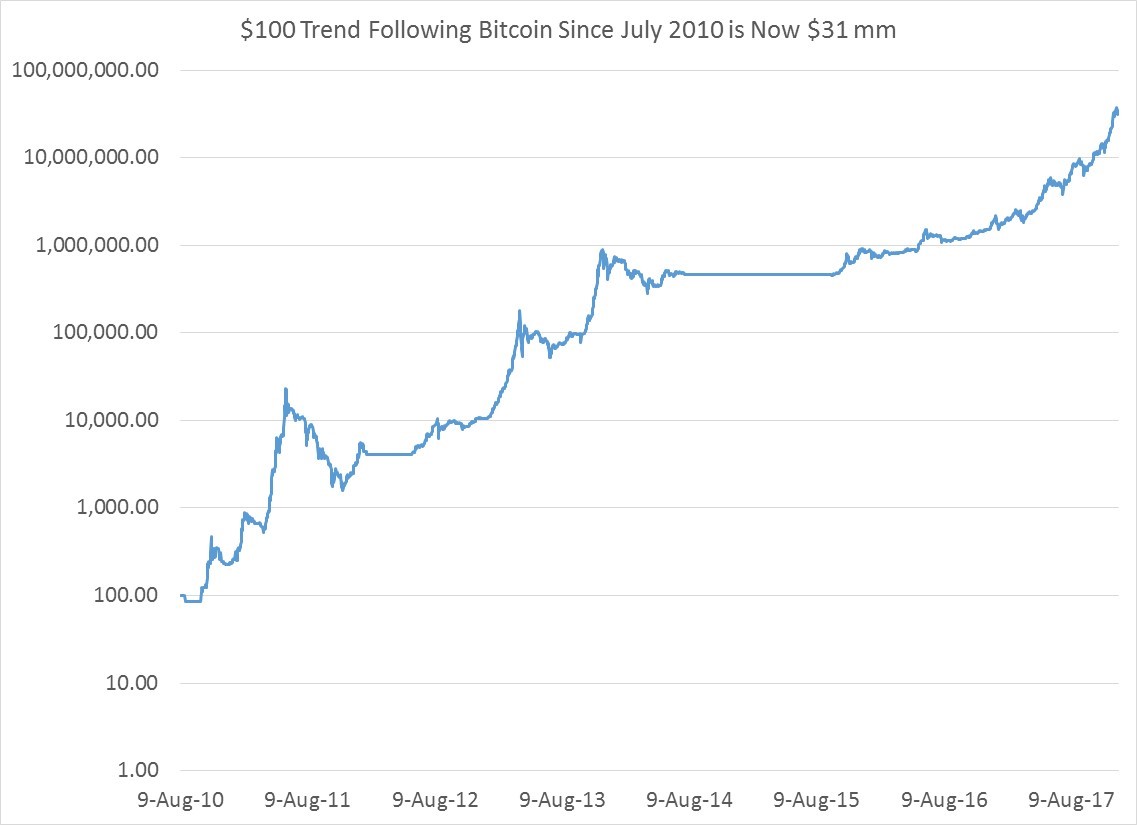

One thing Bitcoin does do consistently is trend, so an investor may consider a tactical timing strategy built around some such rules. The rules applied below were as follows: buy bitcoin if it has been up over the last 250 days, and for the first year when 250 days were not available, buy it if Bitcoin is up over the last month, otherwise don’t hold bitcoin. This turns out to have worked a lot better than buy and hold strategy, since your $100 would be worth $31 million dollars instead of a paltry $17.5 million.

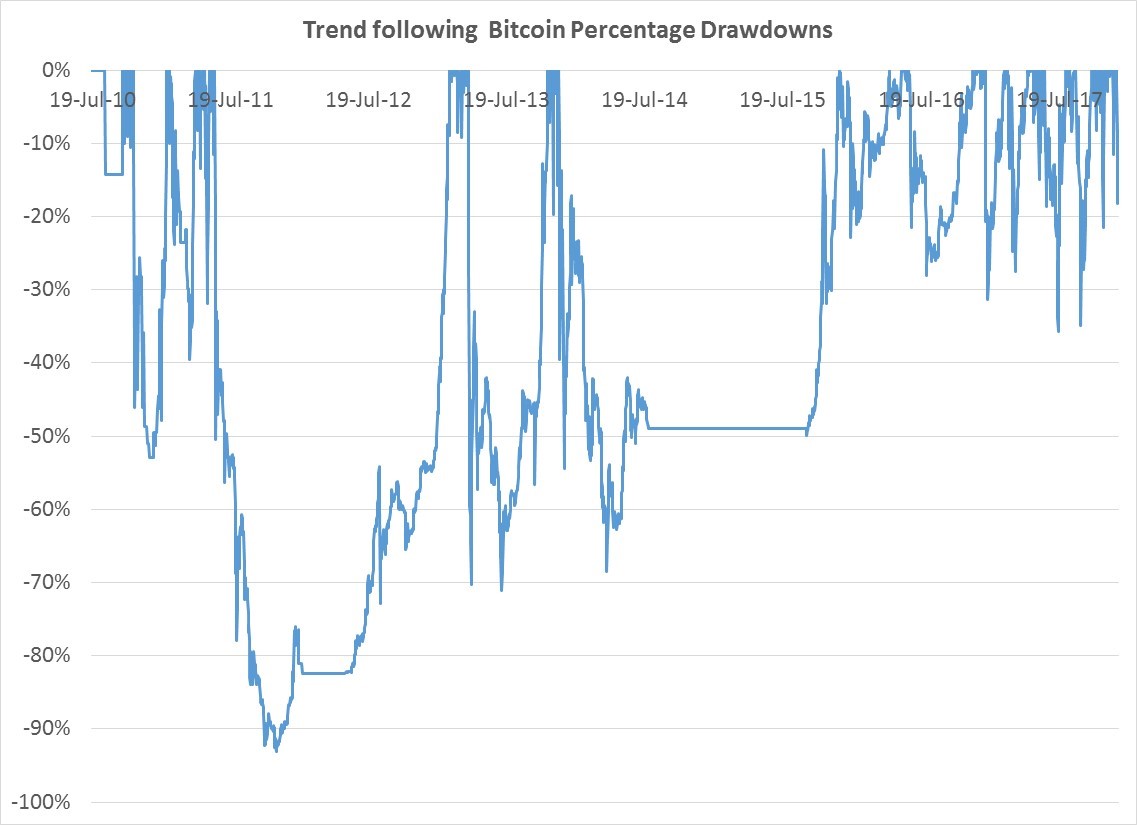

One thing Bitcoin does do consistently is trend, so an investor may consider a tactical timing strategy built around some such rules. The rules applied below were as follows: buy bitcoin if it has been up over the last 250 days, and for the first year when 250 days were not available, buy it if Bitcoin is up over the last month, otherwise don’t hold bitcoin. This turns out to have worked a lot better than buy and hold strategy, since your $100 would be worth $31 million dollars instead of a paltry $17.5 million. And the ride on the downside, while less horrific than a buy and hold strategy, was still rather violent and scary since you still lose 90% of your money at one point.

And the ride on the downside, while less horrific than a buy and hold strategy, was still rather violent and scary since you still lose 90% of your money at one point. Whether Bitcoin will continue to soar and offer buy and hold investor or trend followers the same spectacular returns is unknown. What seems certain is the volatility of 79% annualized will probably be the norm for awhile.

Whether Bitcoin will continue to soar and offer buy and hold investor or trend followers the same spectacular returns is unknown. What seems certain is the volatility of 79% annualized will probably be the norm for awhile.