Last week we looked back through US and several developed countries financial history to see what effect of a 1% annual gain in short term interest rates had upon subsequent equity returns. The results showed that US equities have a fairly negative outlook over the next 4-6 months from an interest rate history perspective. This week we are going to be applying the same test to see the effect on long bond returns. Unfortunately, the news is also bearish for expected long bond returns for the next 4-6 months.

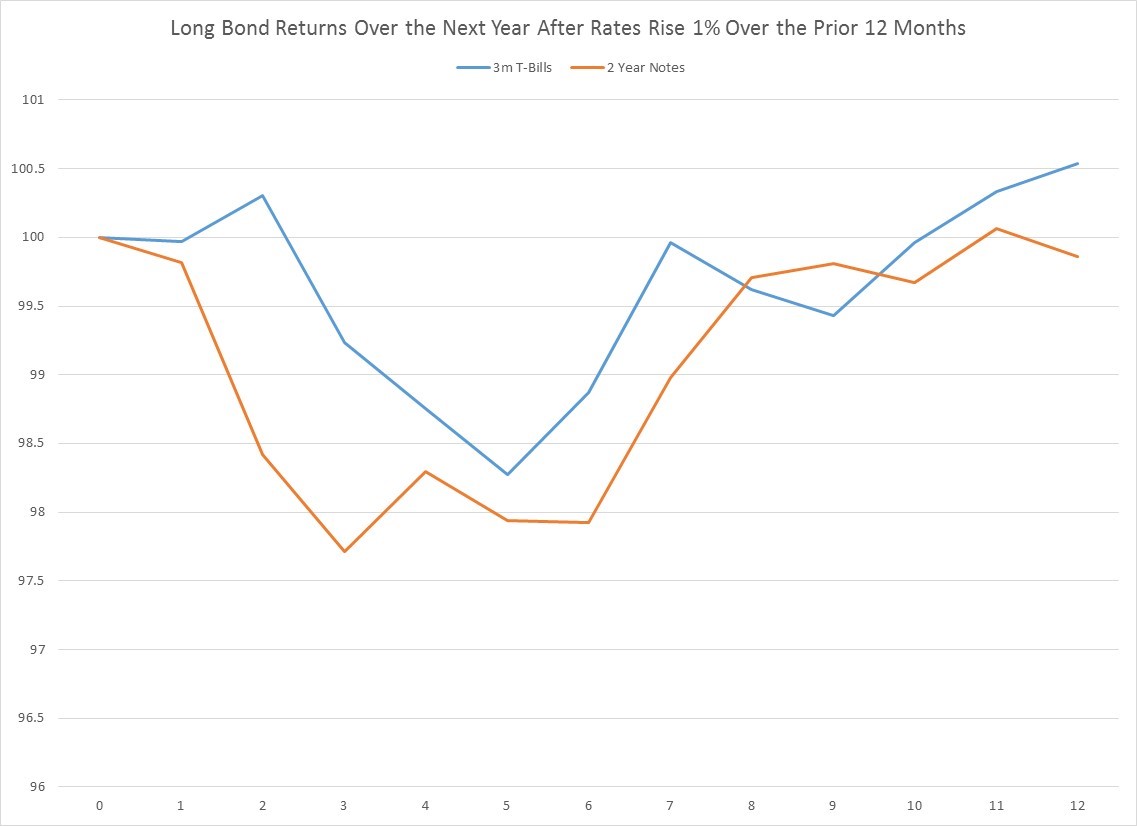

As noted last week, 3-month T-Bills have experienced annual changes of 1% or greater 21 times since 1960, while 2-year notes have seen 28 such increases. The first chart below shows what has happened to US long bond returns (meaning Treasuries of around 20 year maturities) over the next year. Like stocks, negative returns seem to bottom around 4-6 months out, with losses of 1.5% to 2% being highly probable if the past is any guide. Though 1 year later, the pain is over and you are back to flat. Whether US bond investors should expect this bond bounce back to repeat itself this time remains a question mark for me, however. Keep in mind that interest rates and bond yields have been in secular decline since their peak in the early 1980s, and there are a lot of tells of future inflation looming on the horizon at present.

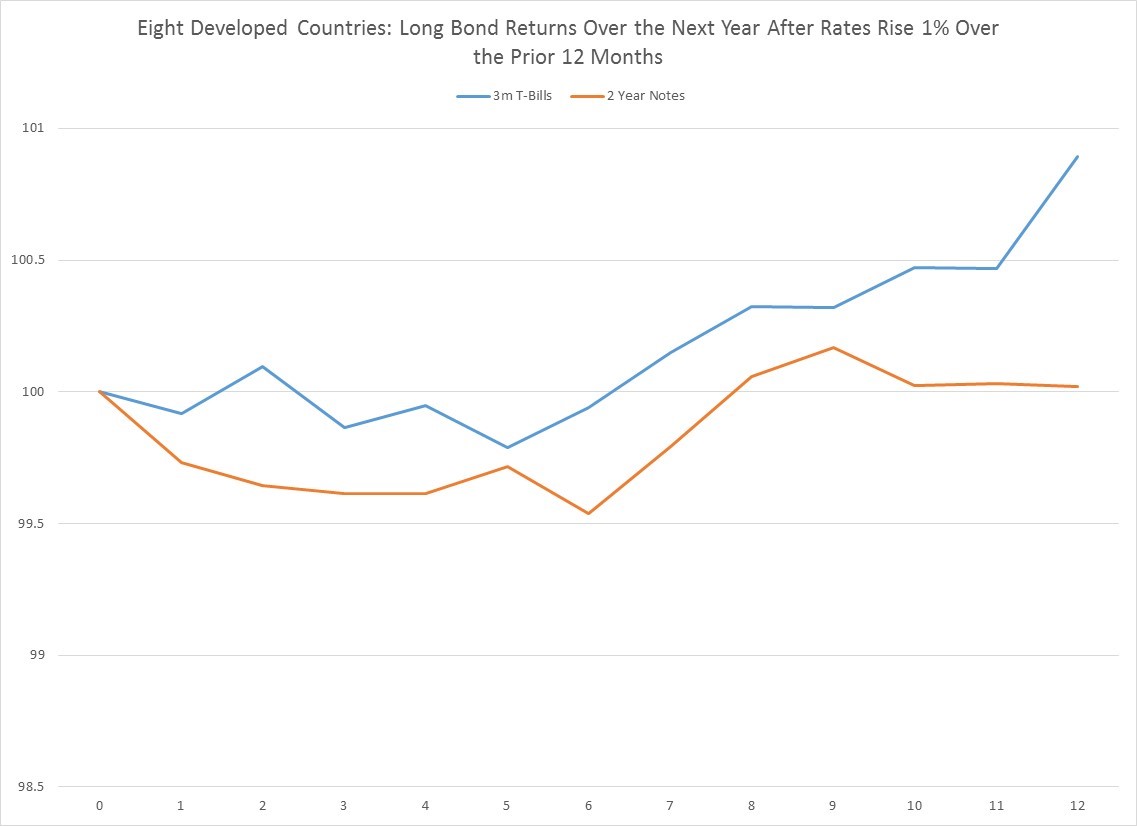

Extending the same analysis more globally to 8 developing major countries, we can see a similar pattern, though with more sample size. Internationally, 3-month T-Bills have shown annual changes of 1% or greater 114 times since 1960, while 2-year notes have experienced 121 increases. Like in the US, the long bond’s maximum losses happen about 5-6 months out, but it’s worth pointing out that the loss is a much more modest 25-50 basis point decline. And also like the US, returns 1 year later are flat and even up.

We will conclude the same way we did last week, by pointing out that while the US and Canada have recently experienced 1% annual increases in short-term rates, the rest of developed world has not. So investing in other developing bond markets outside North America remains a very attractive relative value proposition for the next 4-6 months.