A slightly different version of this post, written with Chris Shuba and Joe Mallen of Helios Quantitative appeared here: IRIS

You are a US investor that wants to deploy some of your money overseas. You think international developed market stocks are attractive relative to US stocks, and you also think the US $ will decline over the period you intend to hold your investment. Your investment decision is logical to you. But you have choices: You could a) simply invest in a traditional index like the MSCI EAFE, b) invest in a fund that systematically emphasizes a particular factor like a value fund that only buys cheap overseas stocks, or c) invest in a developed fund that blends several factors together, like the JPMorgan Diversified Return International Equity ETF (JPIN). What is the best choice?

Investing in a traditional international market capitalization index like the MSCI EAFE is not a bad choice. It has delivered nice returns for a US investor, especially uncorrelated outperformance in the 1970s and 1980s, and helped to diversify a US-only portfolio.

Your second choice is to invest in one particular investing style because it makes sense to you. You might believe that a fund or index that chooses the cheapest or most attractively valued stocks based on metrics like Price to Earnings (PE) is best.

You could go find a discretionary portfolio manager who only buys stocks he deems to be cheap. Typically the concept of “cheap” is based on some absolute metric that the manager has in mind, such as never buying a stock with a PE greater than 15. If there are not enough stocks that are attractive, he will hold his money in cash until he finds the prudent bargains he seeks. This prudence also obviously risks possible underperformance from being absent from the market.

The alternative is to buy a value index or fund that systematically only buys the cheapest stocks in a particular investment universe. So if there are 1000 investable stocks available, the index ONLY buys the cheapest decile of 100 stocks and is always fully invested in the 100 securities that are relatively cheapest. This is an investment approach that a discretionary manger may disdain. The discretionary value manager may look at those same 100 stocks and think they are pricey. But nevertheless, academic research has shown that always being fully invested in the relatively cheapest percentiles of stocks in the US has produced superior returns over many decades.

Such a portfolio is called a “factor” portfolio. Why the name? In the early 1960s, academics introduced the concept of beta and demonstrated that individual US stocks had sensitivities to, and were driven by, movements in the broad market. In the early 1990s, academic research began to show that other “factors” such as value and size also drove US stock returns. Since then, several factors have been identified as driving individual stock outperformance: value, size, volatility, momentum and quality. Stocks that are cheaper, smaller, less volatile, have more positive annual returns and higher profitability have historically outperformed their peers. It turns out these factors also work internationally.

Of all the factors, value is the factor that has been the best known the longest (even before it was academically identified as a “factor”), thanks to the books of Warren Buffet’s teacher Ben Graham. And if you look abroad at an array of developed global markets and create a value index and compare it to its simple market capitalization weighted brother, the historic outperformance of value has been stunning. Until recently.

While there was some variability by country, on average from the mid-1970s up until 2005 a value factor portfolio in a developed market outperformed its market cap weighted index by about 2% a year. That’s a lot. By contrast, since 2005, the average developed country value portfolio has underperformed a market cap indexes by about -40 basis points. Which is the danger of investing in one factor. It may not always work at every point in time.

So if investing in one factor like value runs the risk of underperforming, how about a multi-factor international developed equity portfolio?

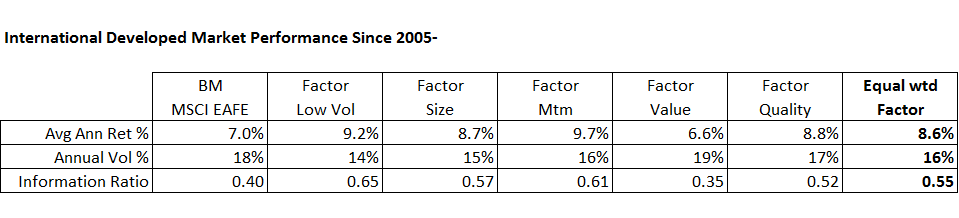

Below is a breakdown of individual factor portfolios’ performance in international developed equity markets since 2005, an equal weighted factor portfolio as well the performance of the MSCI EAFE as our performance reference. Note that, for the last 13 years, value has been the poorest factor by far, while the others have handily beaten the EAFE. An equal weighted portfolio of all 5 factors, while not as optimal as some of the individual factor results, beats the EAFE by 1.6% and has an information ratio, or risk adjusted returns that are superior by 37%. The equal weighted factor portfolio also has the advantage of not having to predict which factor will work when, so even when a factor like value does not beat the market, the other factors can pick up the slack.

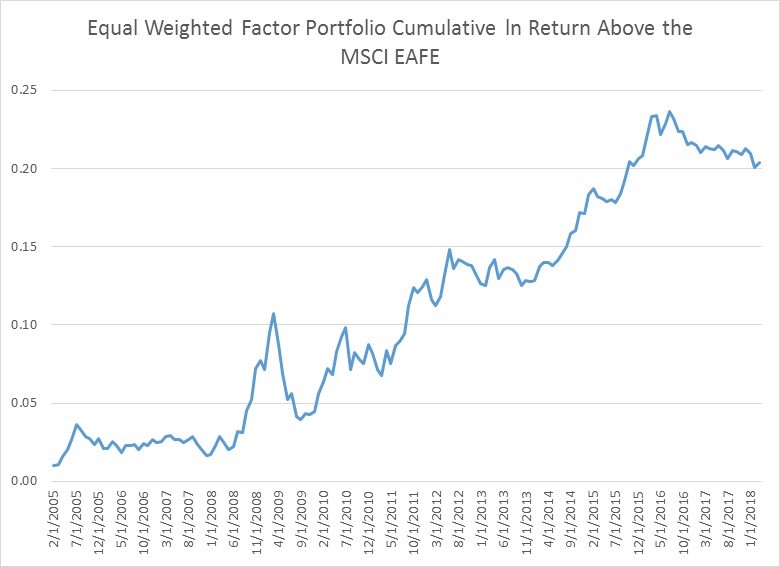

The equal weighted factor portfolio has one other advantage over the market cap weighted alternative. Note in the chart below how well the portfolio outperformed in the 2008 crisis, so it tends to do relatively well in highly volatile sell offs.

While it’s not inconceivable that one or two of these factors could erode, or underperform for a stretch, the fact that you have exposure to multiple factors in a portfolio that seems to do especially well in crises suggest the multi-factor blended portfolio remains the most attractive way to invest in developed markets.