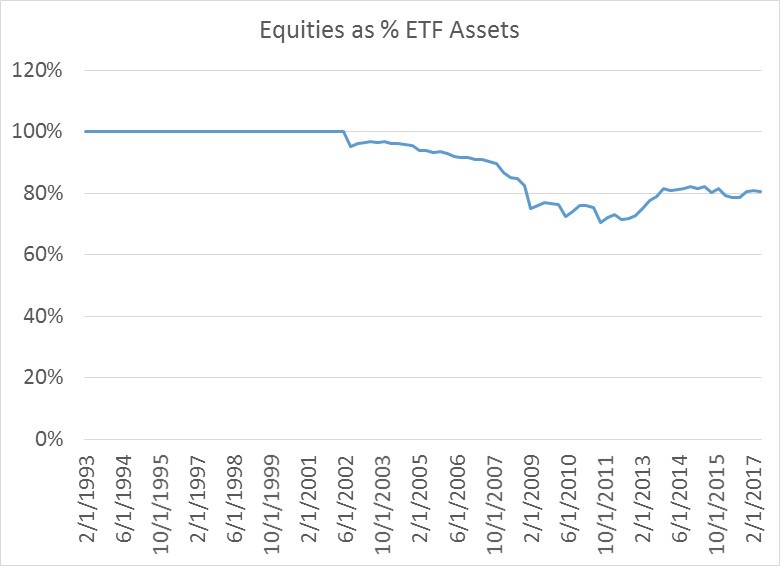

The popularity of Exchange Traded Funds (ETFs) started in the early 1990s as an alternative investment vehicle to Mutual Funds. The first popular ETF, the SPDR S&P 500 (Symbol: SPY) provided investors with inexpensive exposure to the S&P 500 Index. Since that time, ETFs have grown and grown in usage. What is interesting is that despite their proliferation, the majority of ETF assets have been and remain in equities, as you can see in the first chart. For the past decade about 80% of all ETF assets have been in stocks.

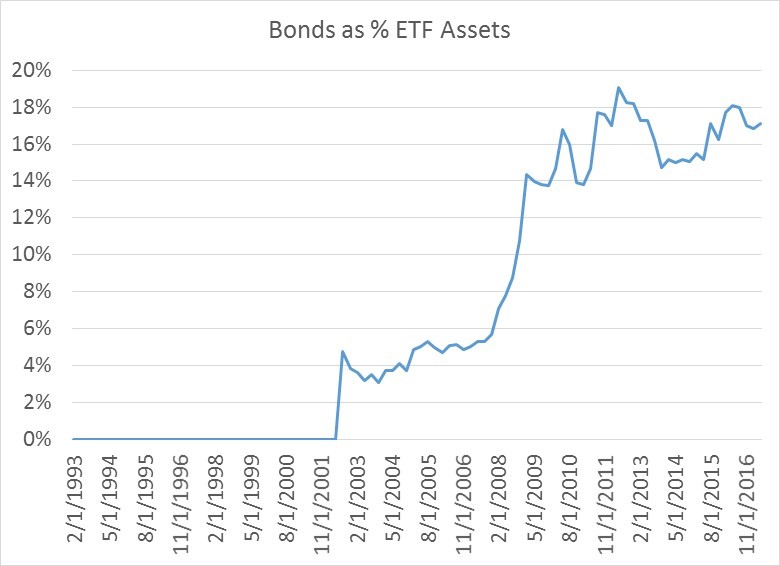

The only asset class that has really begun to crowd them out is bonds.

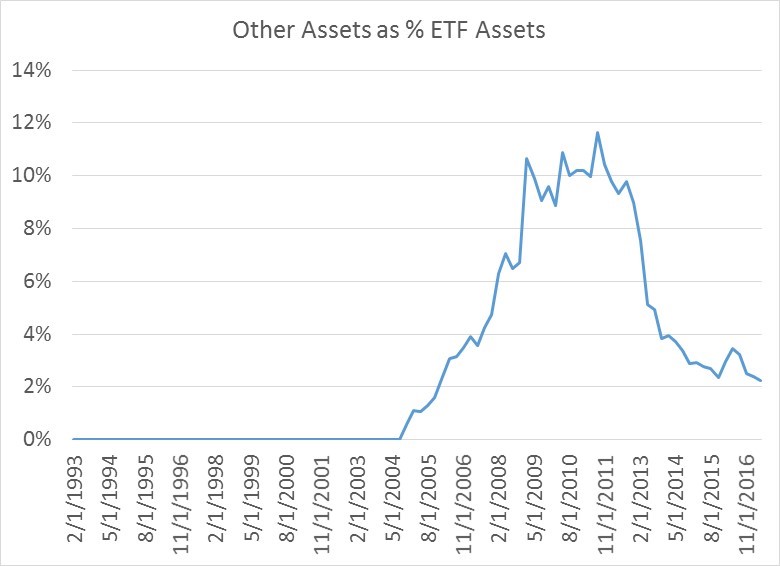

Other investment asset classes and investment alternatives (commodities, currencies etc.) made a decent in-road to total market share from 2008 to 2012 for a period of time, but have since seen their market share decline.

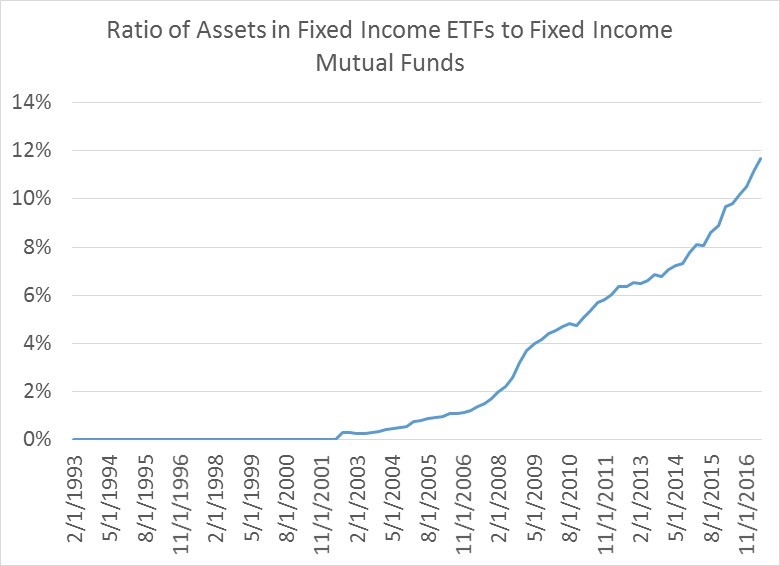

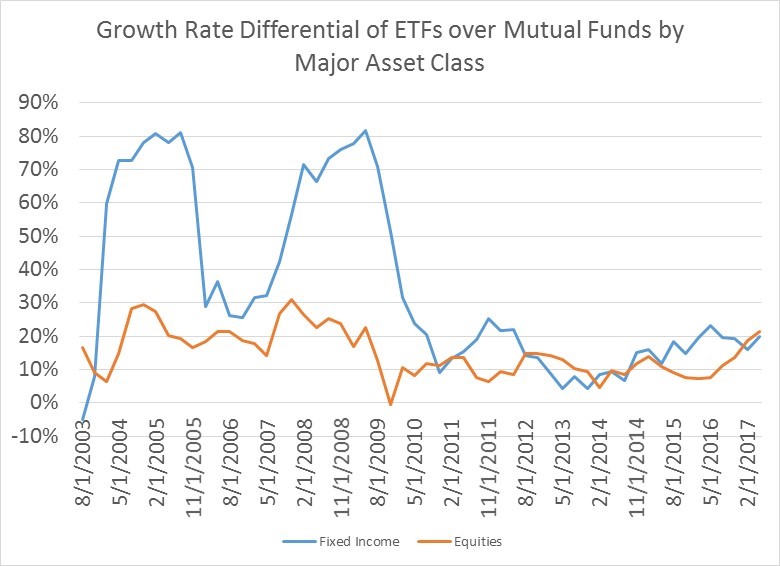

When you look at the market share that ETFs are taking away from Mutual Funds, which on average have loads and much higher fee structures, the relative growth in assets makes sense, especially since many, though not all, ETFs are indexes and not actively managed. That said, there remains plenty of room for ETFs to take greater market share across all asset classes. The first chart below shows assets in Fixed Income ETFs relative to Fixed Income assets in Mutual Funds. Fixed Income ETFs have doubled their market share from 6% to 12% over a five year period, but there is still plenty of market share capacity left.

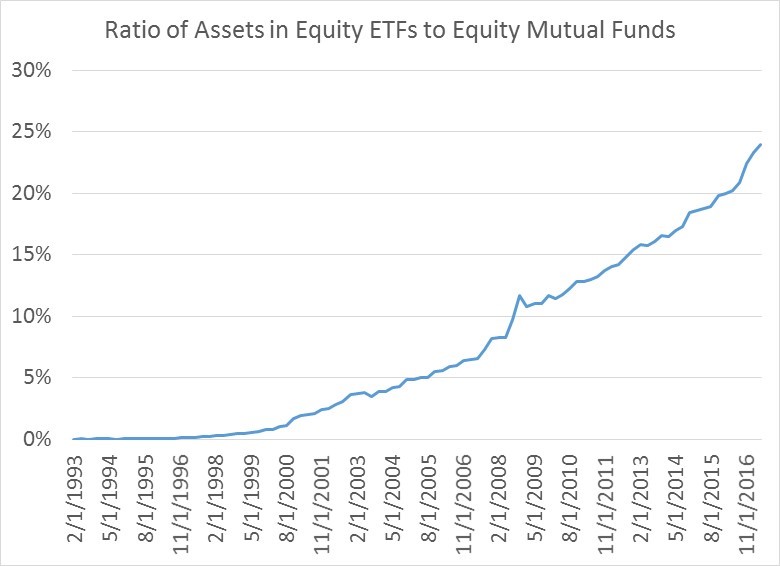

The same story holds for equities. Equity ETFs are now almost 25% the size of equity Mutual Funds. This number has doubled over 10 years.

The growth differential between funds flowing into equity and bond ETFs and those flowing into Mutual Funds remains sizable. Both Fixed Income and stock ETFS are growing 20% faster than Mutual Funds in terms of annual asset growth.

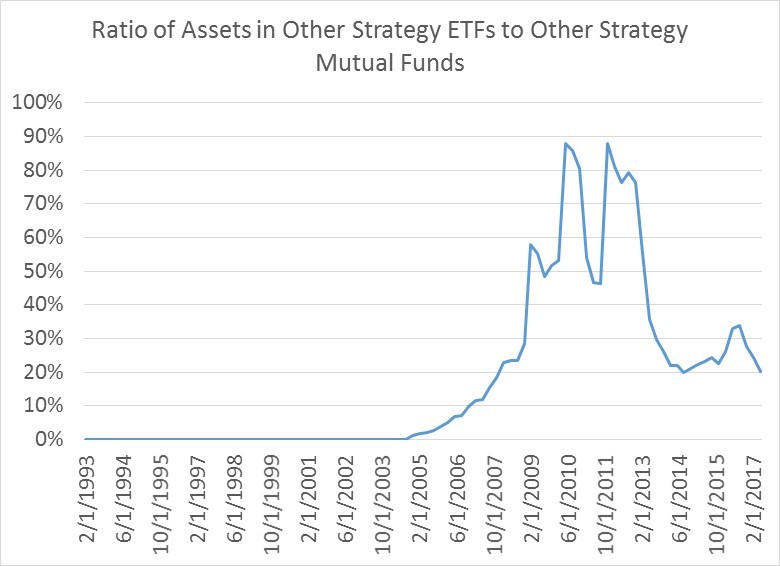

The one area where Mutual Funds still predominate, for the time being at least, is outside of equities and bonds. The majority of non-equity and non-bond assets was actually mostly in ETFs in 2010-2011, but has since moved into Mutual Funds.

I doubt this will continue as the demand for non traditional, alternatives to stocks and bonds grows. Bond yields remain awfully low and equities remain toppy, and the need for investors to find effective diversifiers at minimal cost will eventually drive the creation of low cost ETFs that provide low correlation products to the end user. If we ever get a bear market in stocks again (believe it or not it can happen), expect a boom in the Alternatives ETF space.