There is an old investing adage: “Sell in May and go away,” perhaps created by those who kept their yachts in Newport and wished to summer care free from the vagaries that the stock market brought from June until October. While I lack the poetic wherewithal to create an adage that rhymes and is catchy, there has been a similar kind of under-performance factor in the ETF SPY since since its inception in 1993. Thursday and Friday have offered the investor weak and sub-par returns relative to Monday through Wednesday. Most long only equity traders would be better heading to the beach, gym or golf course on Thursdays in particular.

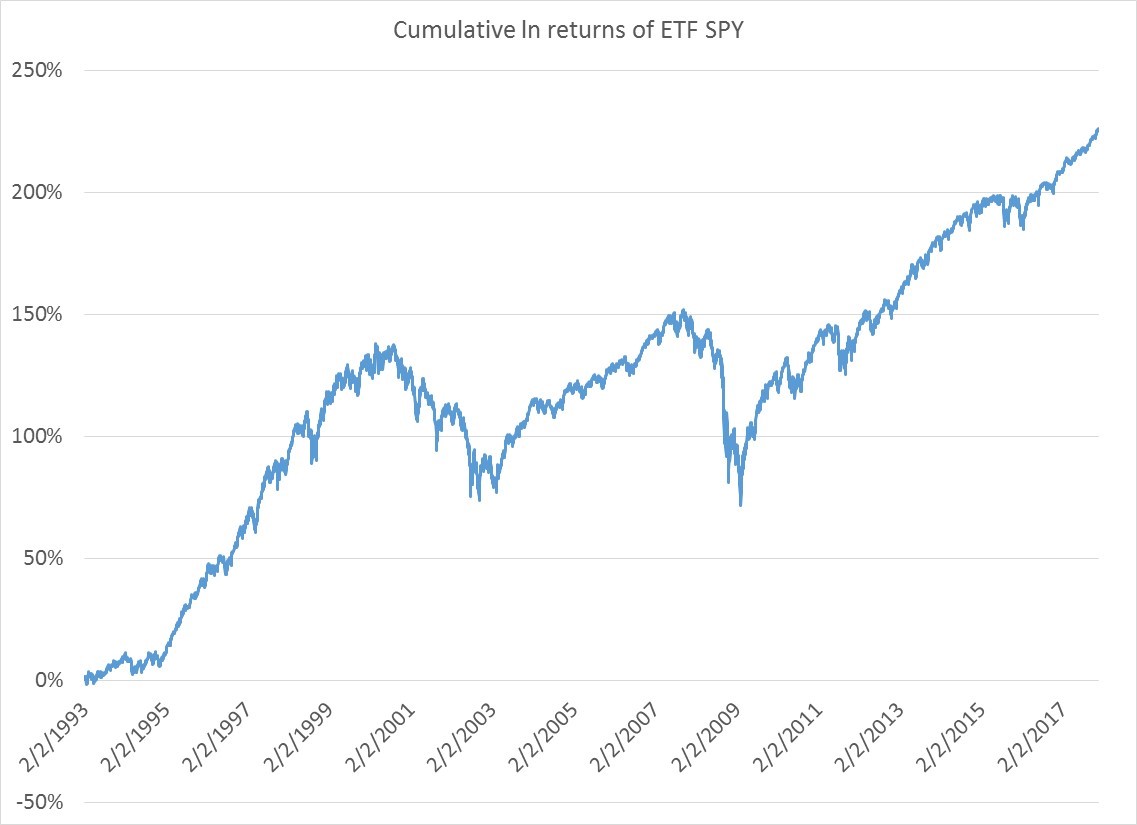

Below is a cumulative natural log chart of the ETF SPY since its inception in 1993. Two bear markets and one long bull market recently.

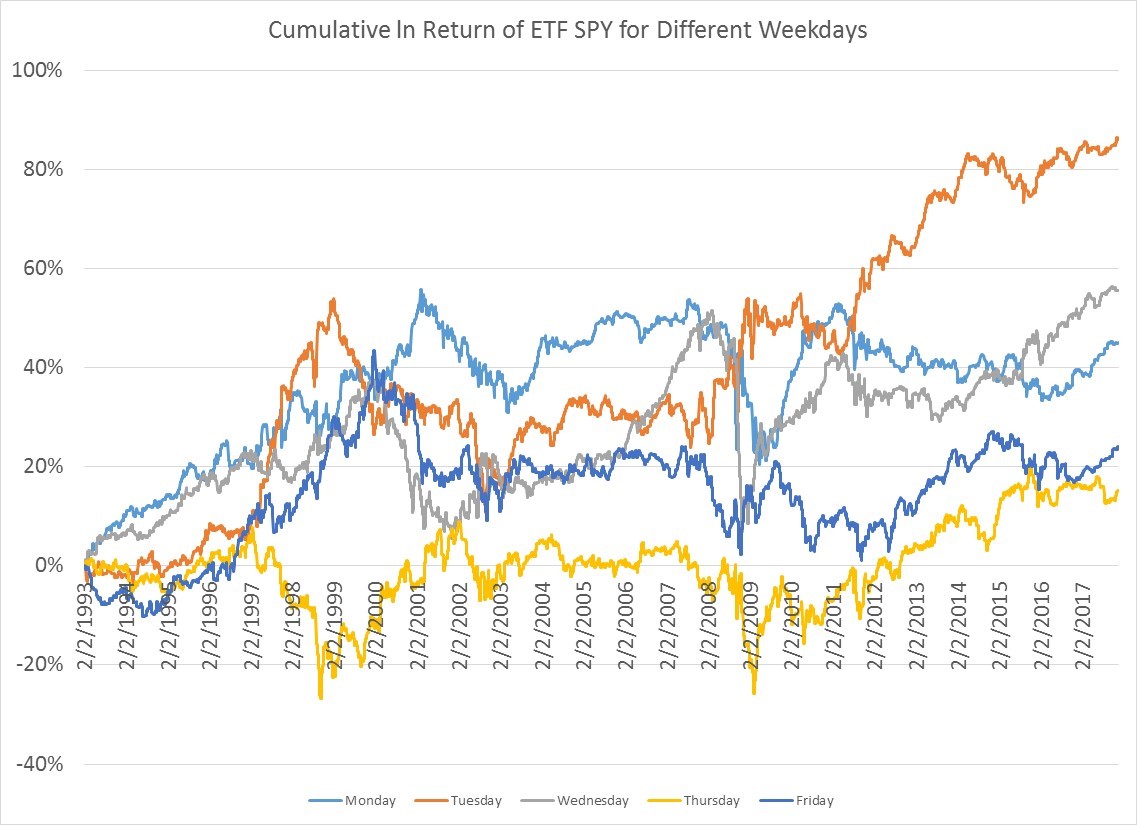

The next chart shows the cumulative ln returns of holding SPY close to close on all five weekdays. That chart by itself doesn’t tell you that much other than that trading any one weekday is a bit noisy.

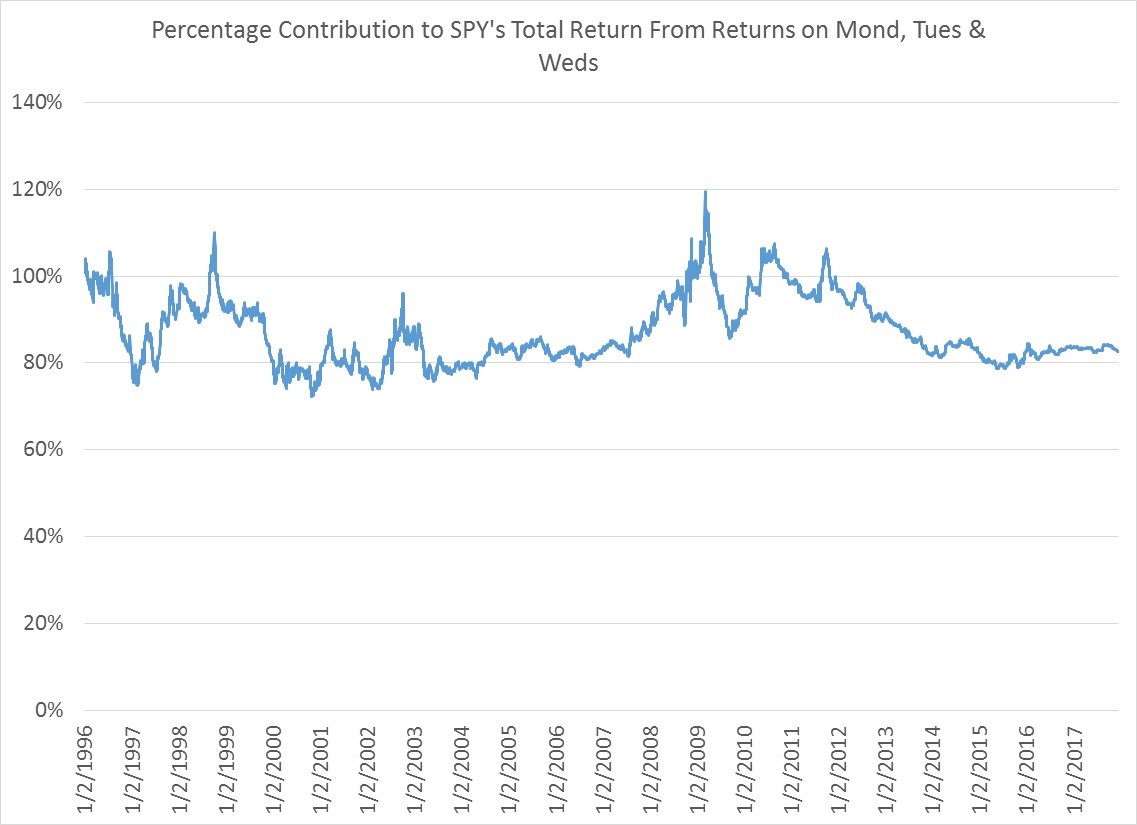

Its when you group days together that the story gets interesting. Below you can see how much of SPY’s positive return through time has come from the first three days of the week on a percentage contribution basis. The way to read this chart is simple: if the SPY gained 100% cumulatively over a 15 year period a reading of 95% would indicate that 95% of the total 100% cumulative return came from M-W and only 5% from Thurs and Friday. As you can see, over the past few years 83-84% of the cumulative returns for SPY since 1993 has come from Monday, Tuesday and Wednesday. At times, because other weekdays like Thursday and Friday were net detractors from cumulative returns, their contribution actually has exceeded 100%, especially during the financial crisis.

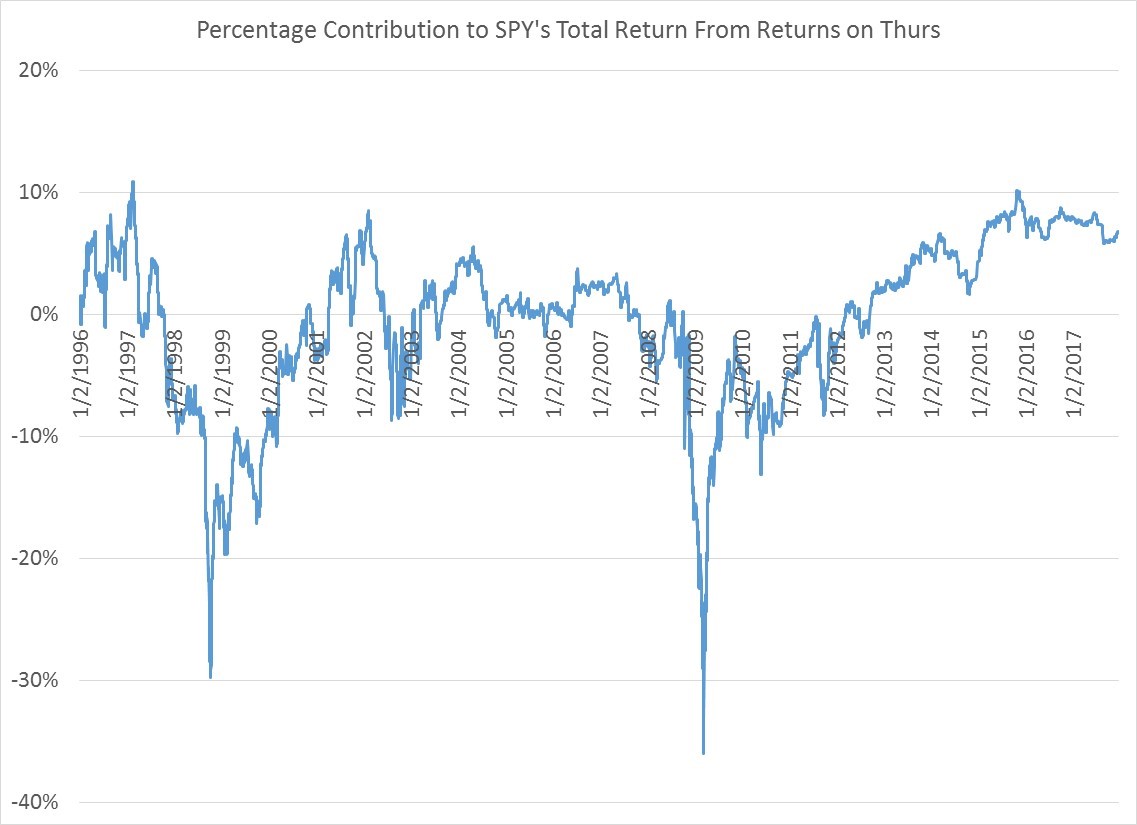

Finally, if you believe in day of the week seasonality, you should close up shop Wednesday night go away on Thursday. As you can see in the final chart, Thursdays detracted massively from SPY’s cumulative returns during the last 2 bear markets. Historically only 7% of SPY’s cumulative positive returns since 1993 have come from Thursdays.