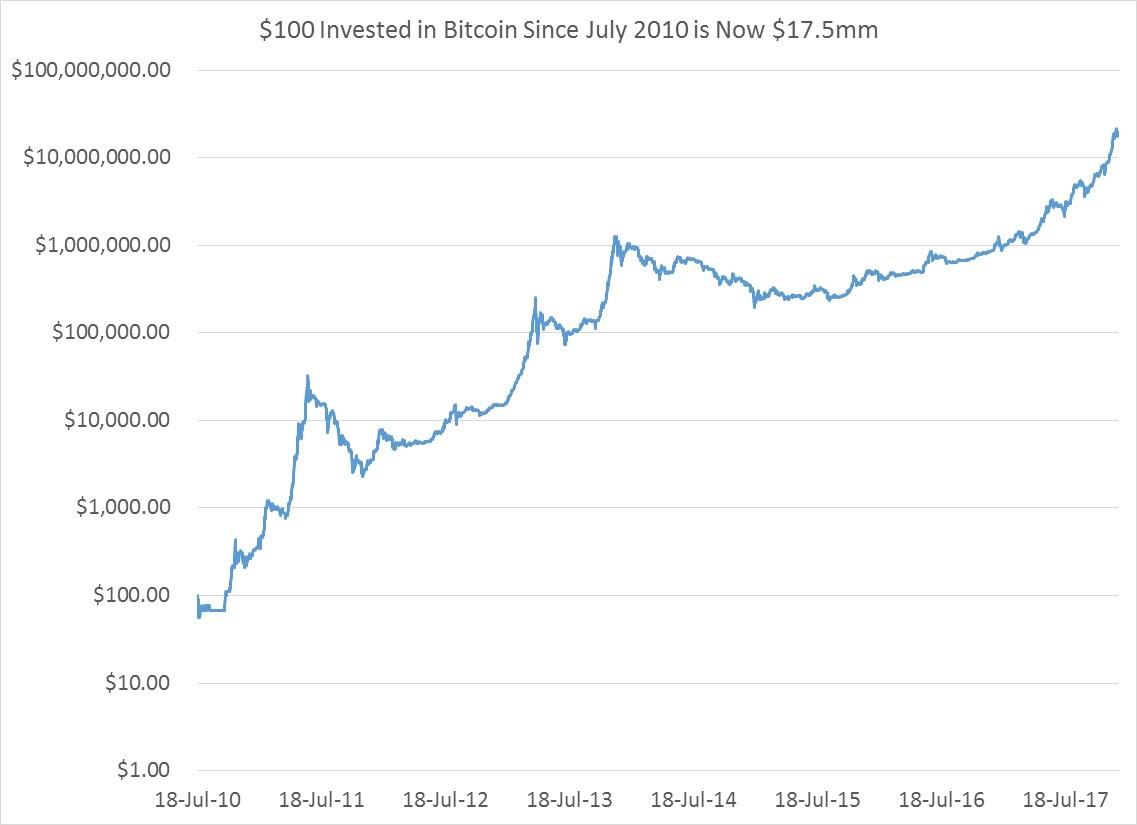

Bitcoin, along its blockchain brethren, is an interesting, relatively new instrument that has emerged from utter obscurity. When two different exchanges are rushing to launch a new financial future, a hedge fund you interviewed with has abandoned its other investments to focus solely on bitcoin, and governments are shutting off access to a market, you know a market is HOT, but also not fully understood or trusted. Whether crytpocurrencies are in the long-run a legitimate alternative to sovereign currencies or centuries old stores of value like gold and silver is another question. It is, as many new technologies and instruments are prone to be, an object of intense speculation. Calling this is a bubble or a mania is semantics. Gauging the levels of dumb money or retail participation is difficult because of the lack of centralized exchange and public information about who is buying. Nevertheless, the price swings are huge, and the historic losses have been awful. But if you were an early investor, or miner who held on, the rewards were incredible.

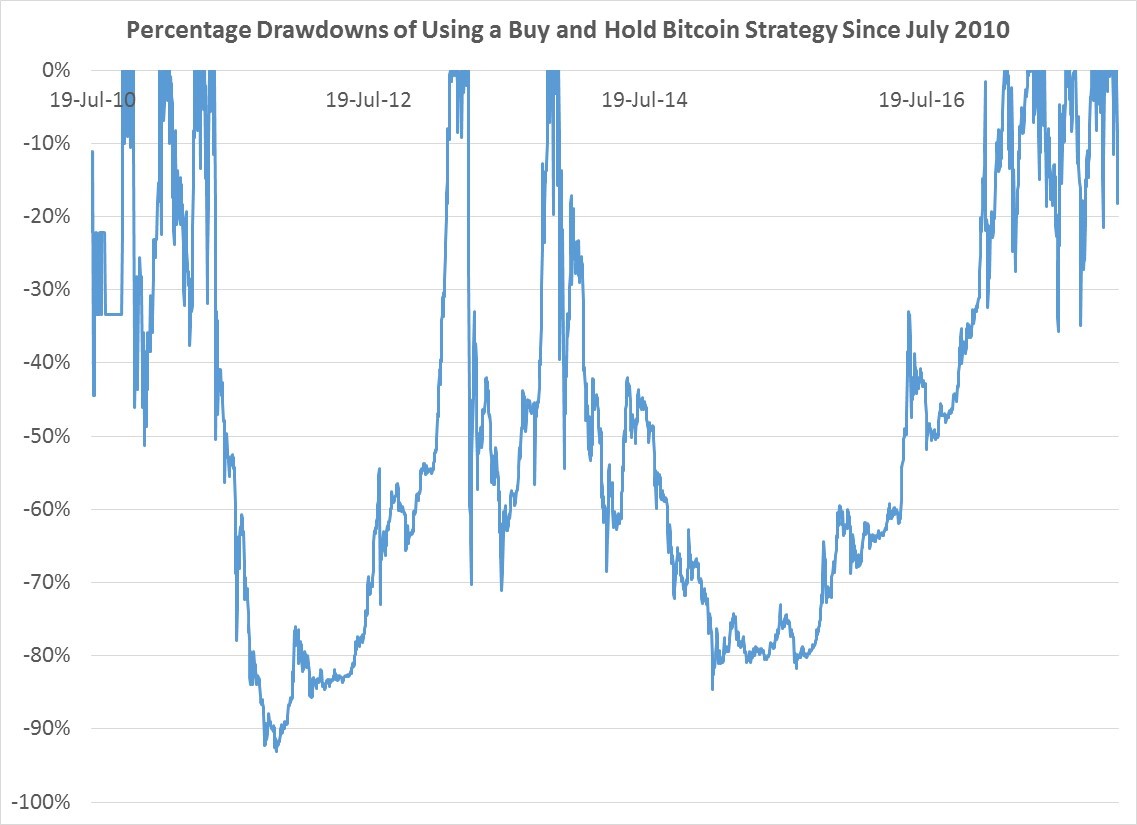

But those returns, shown in the chart above, assume you stood the course, because it was a rough, rough ride as you can see in the next chart. Losses of 80% and 90% of your investment were simply the norm. Expect the same in future.

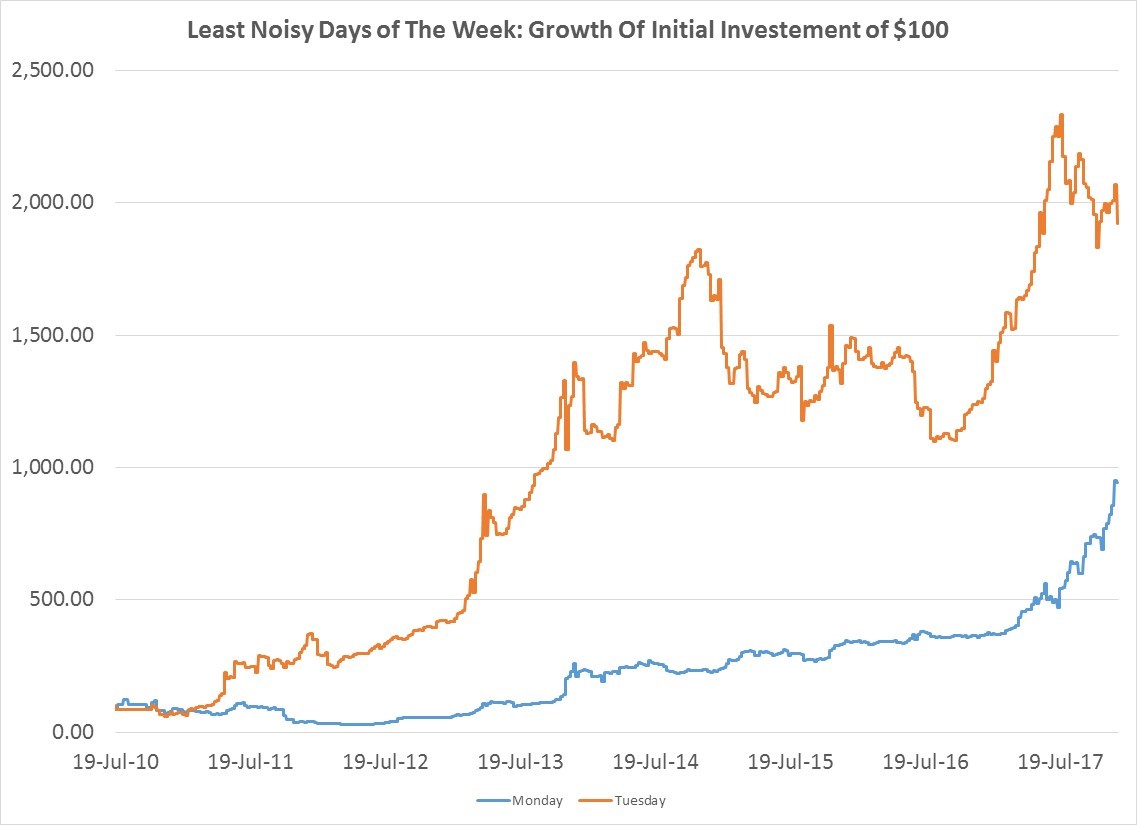

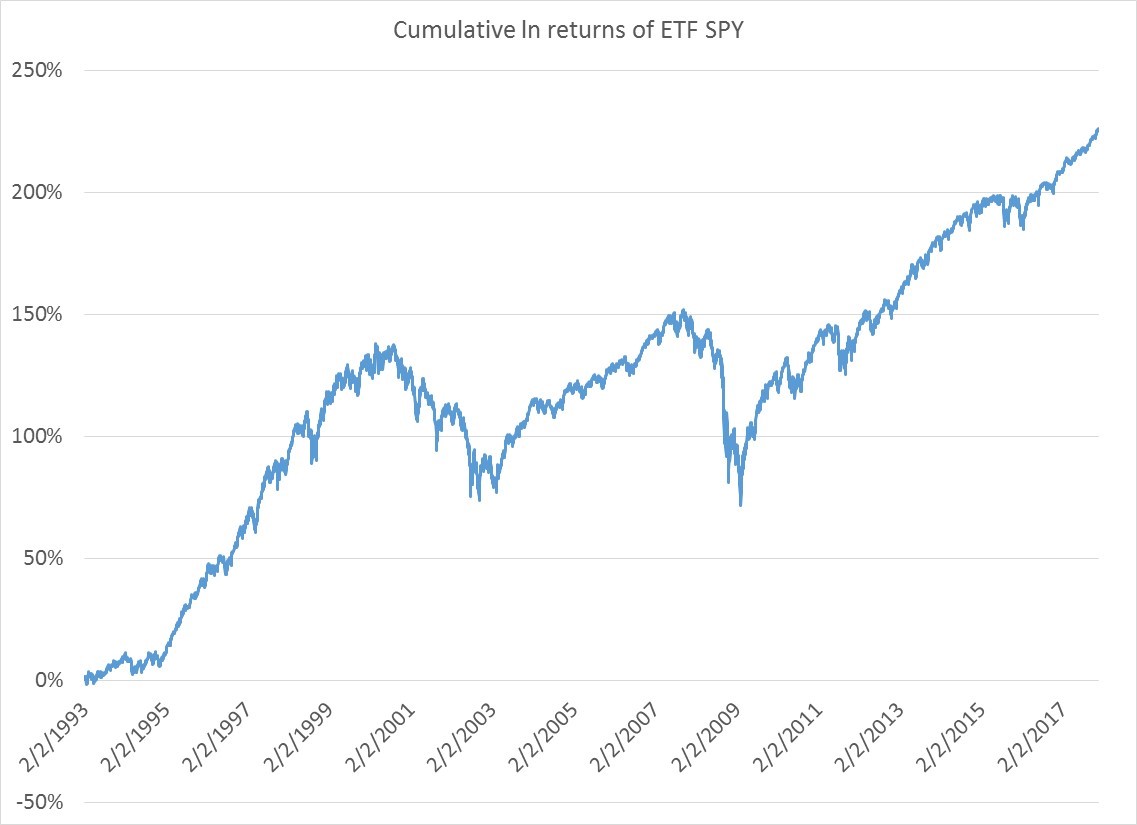

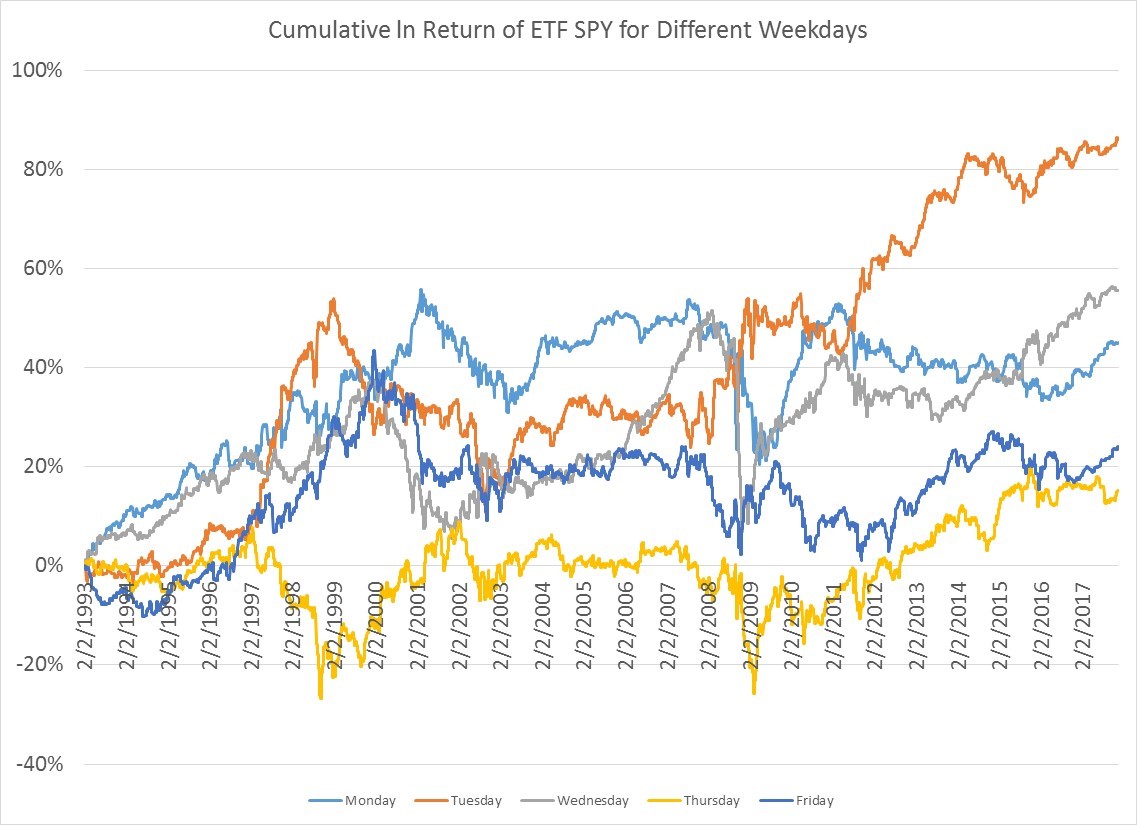

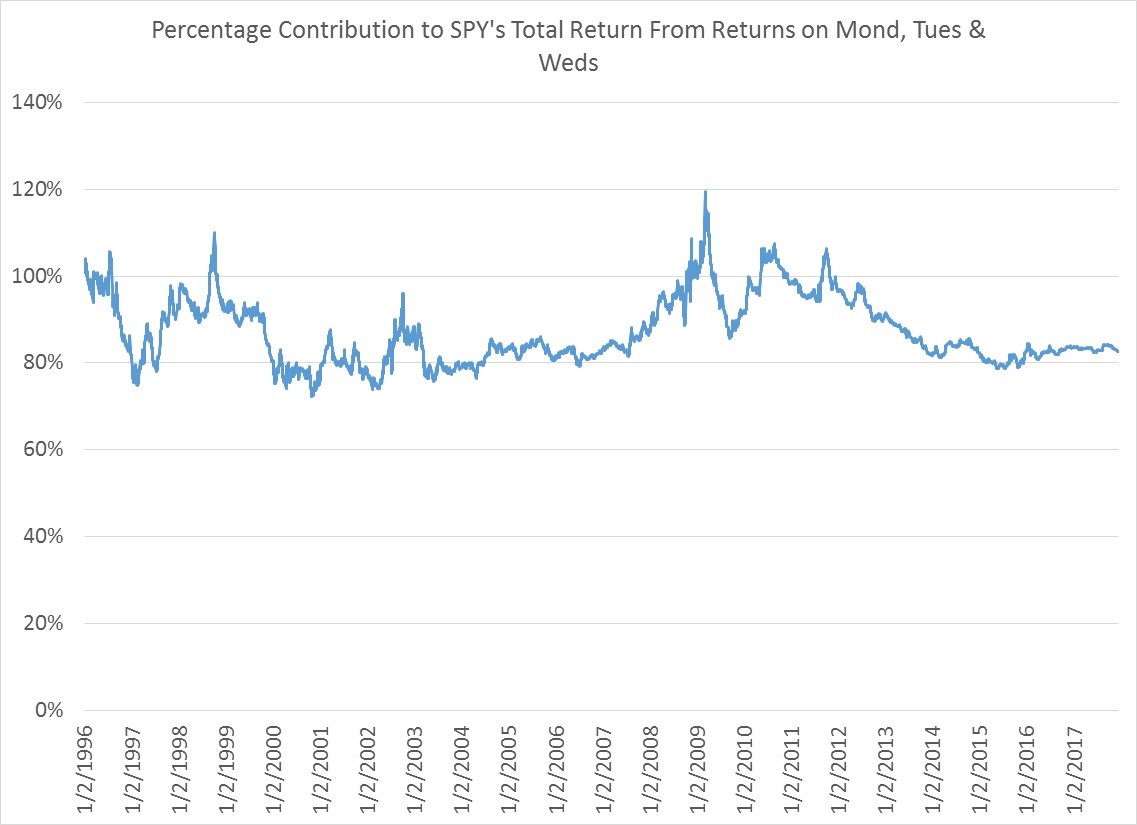

Since there is little data at this point, we don’t really have enough sample size to get any meaningful numbers on monthly seasonality. When you dig into daily seasonality, you don’t see a ton either. Its noisy, though as you can see in the next chart, Tuesdays and to larger extent Mondays have tended to be days that Bitcoin goes up most consistently.

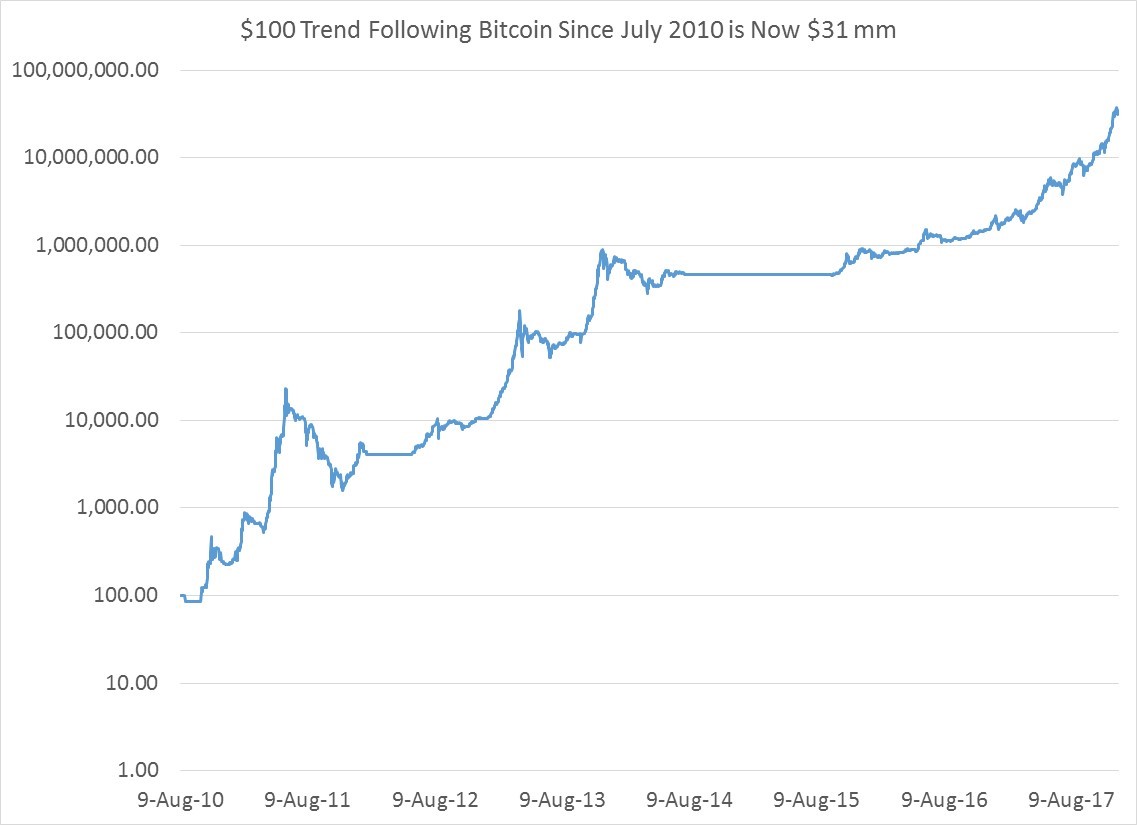

One thing Bitcoin does do consistently is trend, so an investor may consider a tactical timing strategy built around some such rules. The rules applied below were as follows: buy bitcoin if it has been up over the last 250 days, and for the first year when 250 days were not available, buy it if Bitcoin is up over the last month, otherwise don’t hold bitcoin. This turns out to have worked a lot better than buy and hold strategy, since your $100 would be worth $31 million dollars instead of a paltry $17.5 million.

One thing Bitcoin does do consistently is trend, so an investor may consider a tactical timing strategy built around some such rules. The rules applied below were as follows: buy bitcoin if it has been up over the last 250 days, and for the first year when 250 days were not available, buy it if Bitcoin is up over the last month, otherwise don’t hold bitcoin. This turns out to have worked a lot better than buy and hold strategy, since your $100 would be worth $31 million dollars instead of a paltry $17.5 million.

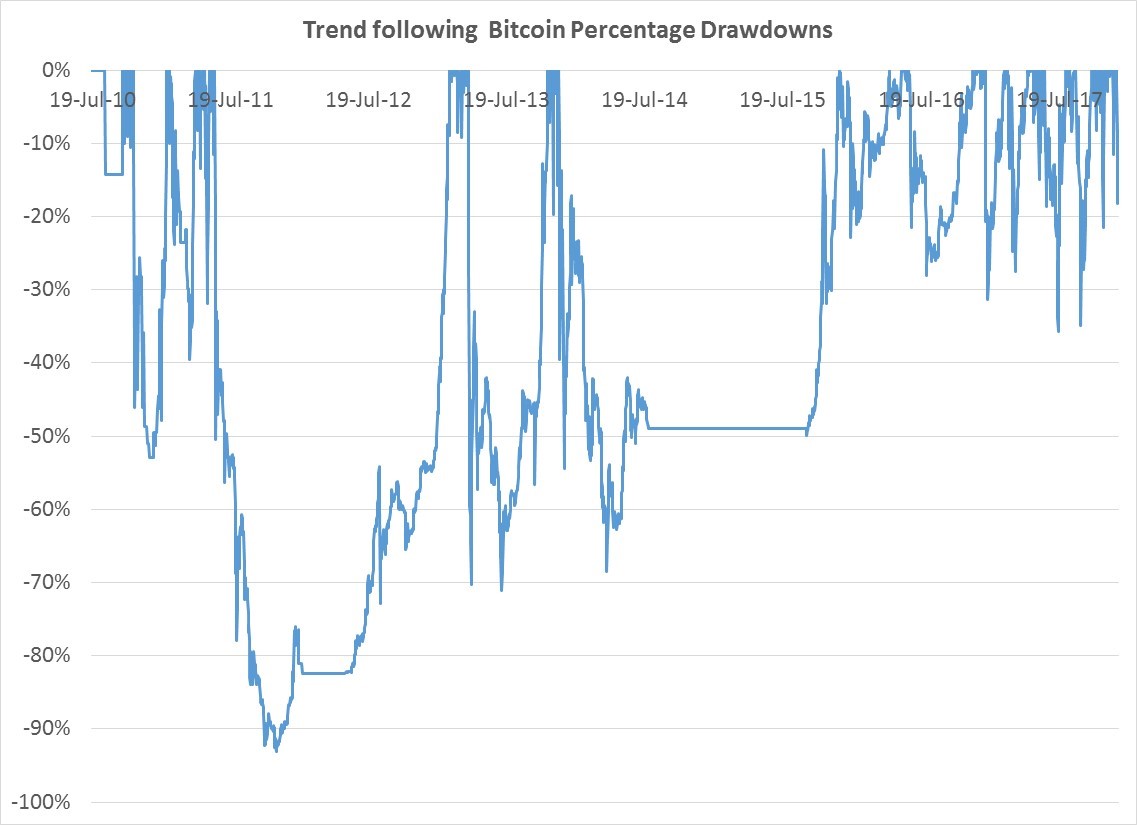

And the ride on the downside, while less horrific than a buy and hold strategy, was still rather violent and scary since you still lose 90% of your money at one point.

And the ride on the downside, while less horrific than a buy and hold strategy, was still rather violent and scary since you still lose 90% of your money at one point.

Whether Bitcoin will continue to soar and offer buy and hold investor or trend followers the same spectacular returns is unknown. What seems certain is the volatility of 79% annualized will probably be the norm for awhile.

Whether Bitcoin will continue to soar and offer buy and hold investor or trend followers the same spectacular returns is unknown. What seems certain is the volatility of 79% annualized will probably be the norm for awhile.

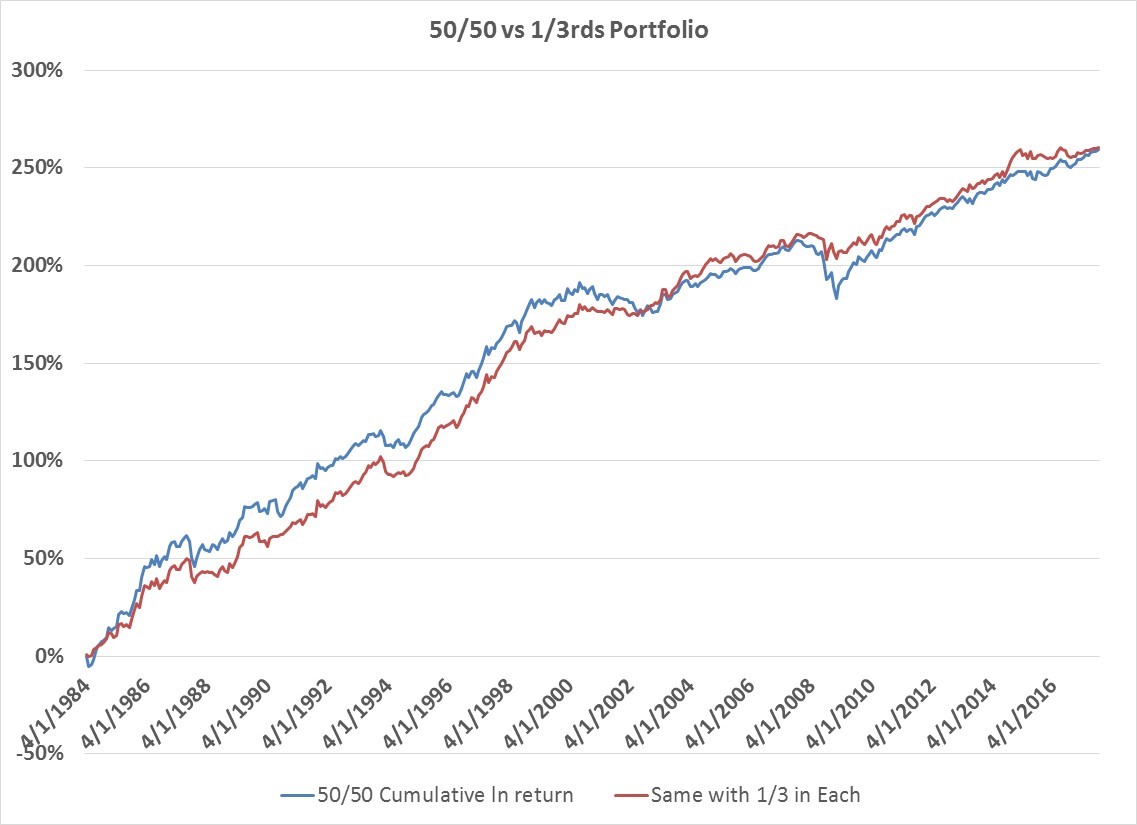

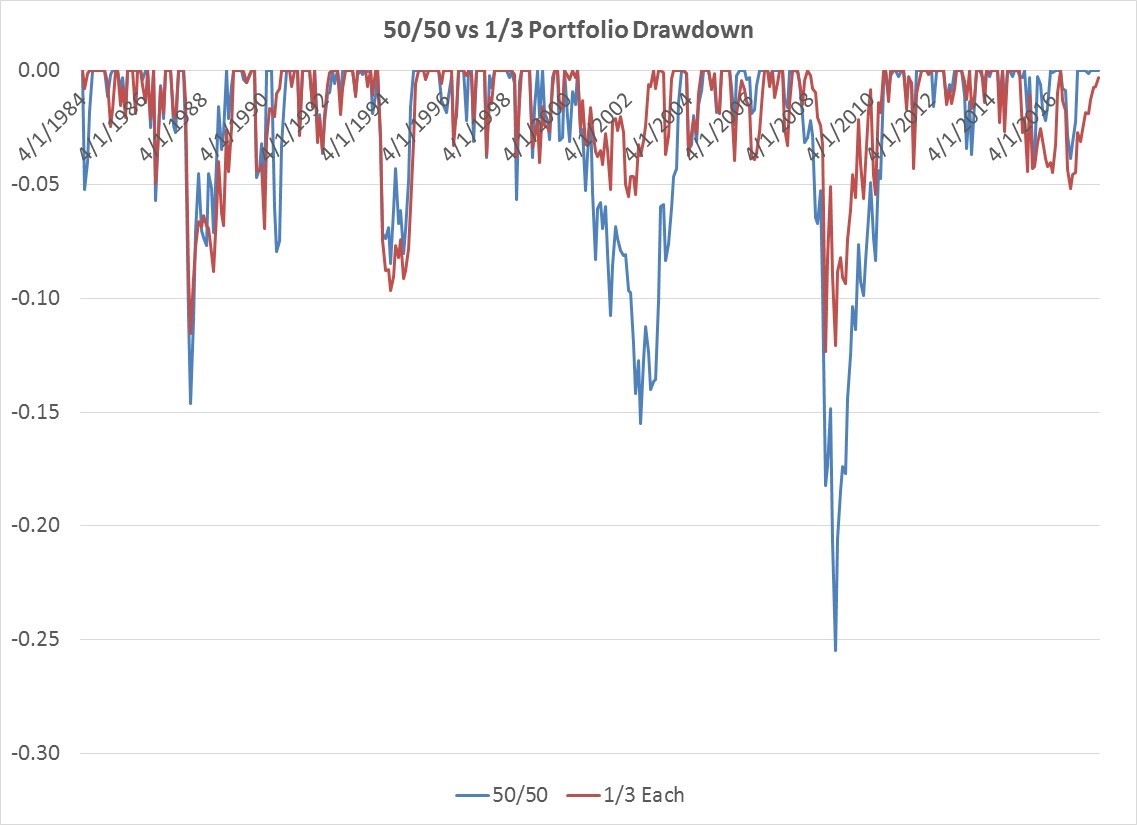

There are other ways of slightly improving the portfolio blend—you could add more than 4 futures to your managed futures strategy for further diversification. Similarly, a risk parity version of the 1/3 portfolio that equalizes volatility among all 3 strategies improves your risk-adjusted returns and brings your max % loss down to -10.4% from -12.4%.

There are other ways of slightly improving the portfolio blend—you could add more than 4 futures to your managed futures strategy for further diversification. Similarly, a risk parity version of the 1/3 portfolio that equalizes volatility among all 3 strategies improves your risk-adjusted returns and brings your max % loss down to -10.4% from -12.4%.